Earlier this week, Kyle Bass spoke on Bloomberg about the reckless expansion of the credit system in the Middle Kingdom.

He warned about the ballooning asset-liability mismatch in the shady $4-trillion wealth management products (WMPs) market.

And went on to say “this is the beginning of the Chinese credit crisis” while admitting it could take some time for things to really start unraveling.

A fair call…

How many of us have figured the trend out, only to allocate too much capital to a trade and even lose on a trade which finally works… eventually? I know I have. I’m pretty sure Kyle’s position sized pretty well. After all, this is far from his first rodeo.

In the interview Kyle referenced an SCMP article from a few weeks ago that went largely unnoticed by most. It was on the Chinese government coming up with more and more creative ways to stem the capital outflow underway since mid-2014:

“China’s foreign exchange regulator, SAFE, has asked for cooperation from multinationals, including Sony, BMW, Daimler, Shell, Pfizer, IBM and Visa, to manage and control the flow of capital out the country.”

This all feels a bit deja vu-ish.

Long-time readers will know we’ve been bearish on China and the renminbi for well over 2 years now. Back in October 2014 we said that:

“I don’t know exactly how a breakdown in the renminbi will play out. However, it is a sure bet that all those markets that prospered over the last 15 years or so on the back of a China will do badly. Where things become shady is the collateral damage to other markets that have had nothing to do with the Chinese economic miracle.”

A few months later, we took a closer look at the cracks appearing in China’s interbank lending market, indeed feeling (correctly in hindsight – lucky us) that timing had arrived to short the currency cross via the options market:

“The interbank lending market is an integral part of any country’s banking system as it is where banks maintain their short-term liquidity requirements. Often a bank will have a mismatch between between short-term assets and obligations and as such they will have to enter the interbank lending market to maintain optimal liquidity. If a bank has excess short-term reserves they may want to lend these out to other banks who have a shortfall in short-term reserves. The opposite also occurs where a bank, with a short-term funding deficit, will enter the market to borrow funds to match short-term liabilities.

The behavior of the interbank lending market can provide one with a good appreciation for the liquidity of the banking system as a whole. If there is a lot of liquidity in the system (more short term assets than liabilities) the interbank rate will fall, if there is scarcity of short term assets relative to liabilities then rates will rise. So a rising interbank rate is generally associated with contracting liquidity conditions. Rapid rises in interbank lending rates are often associated with banking or credit crisis. This happened in the lead up to the GFC. What happened was that as banks began to fear the ability of other banks, who are their counter-parties, to make good on their obligations they demanded higher rates especially from banks already facing liquidity problems which only compounded their original the situation.

A rapid rise in a country’s interbank lending market is also a good predictor of the direction of a country’s currency, or at worst a confirming indicator. Let’s have a look at the interbank lending market of a few emerging nations over the last 12-18 months and then look at what is happening with the renminbi. I think it is instructive for what we have been positioning for in our funds.”

In truth, it was an easy bet to make.

Volatility was around 2%! NOT buying put options would have been like having Scarlett Johansson invite you into her bed and then falling promptly asleep. You just couldn’t do that. And so you had to buy.

Taking a look at the Chinese interbank lending today:

Not yet getting critical but worth watching.

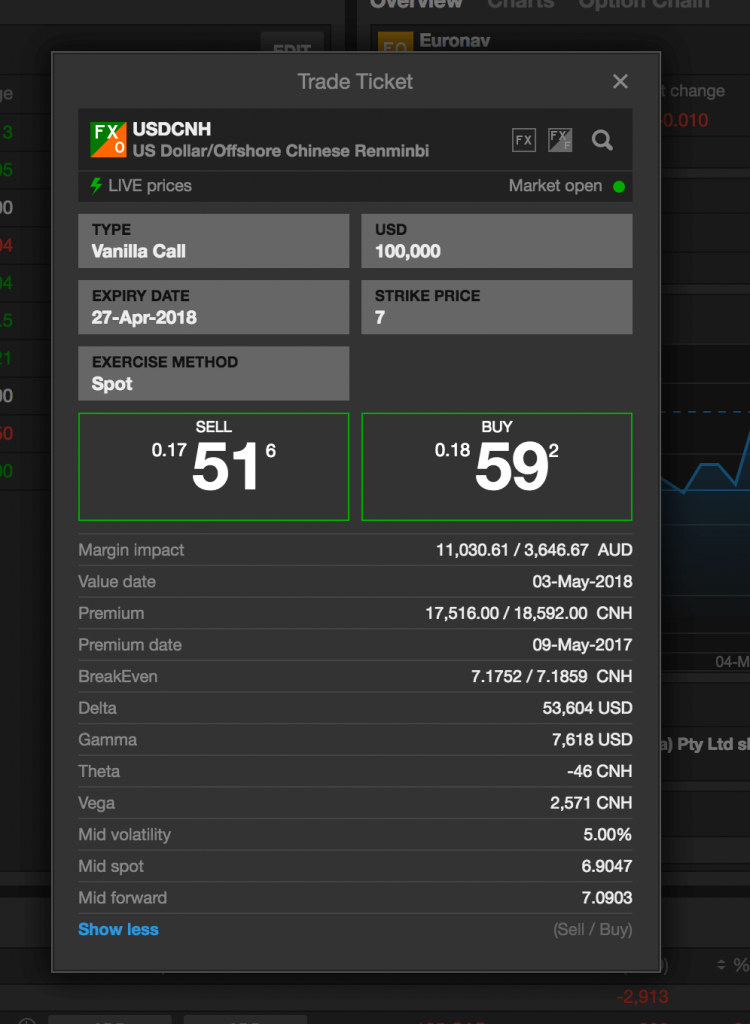

And pricing of the options:

So a 6.6% move to make 100%. Seems reasonable but nowhere near as good as it looked in late 2014 – unfortunately.

The problem – if there is one – is that 12 months is a long time to date an ugly girl, work for a nasty boss, or drive a Lada. But it isn’t a particularly long timeframe to hold an option for.

And yet that’s the best the option market gives us.

Sure, you can throw your towel into the ring in the futures markets but if, like me, you dislike leverage and margin calls (because you WILL get it wrong at some point), then you’re going to have to figure some better way to ride this pony.

The answer, I think, is this.

– Chris

“What you see when the liquidity dries up is people start going down… and this is the beginning of the Chinese credit crisis.” — Kyle Bass