Our subscriber Mark Schumacher recently sent a note to his investors copying me and I felt was well worth sharing.

Mark Schumacher’s Note

Investors,

It is standard practice to diversify portfolios among asset classes with low correlations, which we do, but I have found the benefits of this methodology to be limited. While client portfolios are diversified in this manner with exposure to a variety of asset classes such as equities, currencies, foreign real estate, commodities and gold, we have further diversified by strategy. I am finding the strategy buckets to be more valuable than asset classes when making investment allocation decisions.

Our core competency has been, and will continue to be, centered on gaining early exposure to long-term macro trends. Although this investment strategy exposes us to a good deal of volatility in monthly returns, over a multi-year period it offers an excellent trade-off between risk and reward. For this reason, trend investing will remain our primary strategy, however, its share of the total pie is shrinking as we add other strategies to the mix.

Over the past two years we have broadened our skill set by studying alternative investment strategies in an effort to enhance diversification and long-term returns. While we have researched and tested these methodologies for some time, we are only now starting to incorporate them into our portfolios. Much of our future correspondence will be to explain our chosen strategies and discuss specific investment choices, but for today, I simply wish to introduce you to the concept of diversifying a portfolio by strategy rather than simply by owning different asset class.

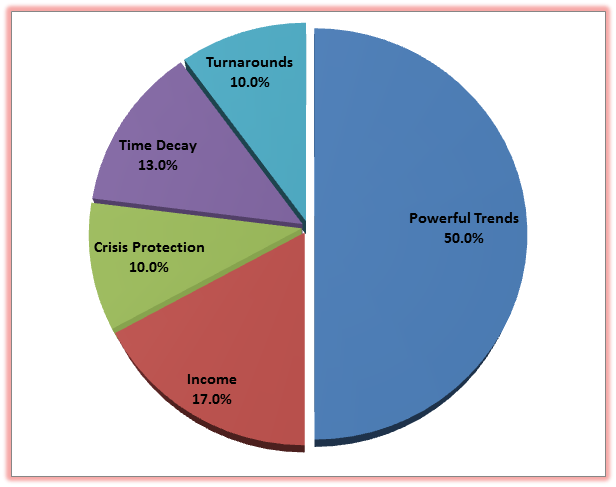

We have categorized these investment strategies into five buckets with some strategy buckets having multiple tactics available to us. These five buckets include our traditional strategies and new ones designed to complement our core strategy of investing in the early stages of powerful trends. Below we outline each strategy and provide a pie chart for a portfolio near the midpoint of our target allocation ranges. Note that the newer strategies represent a minority of our investments and are largely designed to generate income which includes writing covered calls.

Diversification by Strategy

Diversification

Five Strategy Buckets

1. Powerful Macro Trends:

a. Target Asset Allocation: 40% – 60% (for most portfolios).

b. Qualifications: The trend must be 1) powerful – have at least a decade of strong growth remaining subsequent to our initial investment, and 2) macro – big enough to offer multiple publicly traded securities to choose from. All else being equal, if a trend or security under review is different from (mutually exclusive of) other portfolio holdings then it gets extra consideration due to its greater diversification benefits.

c. Time Horizon: 5 – 10 years. Trends are not trading ideas. The above qualifications mean we are looking to own these assets for five years or longer.

d. Volatility/Risk: Volatility will always be high in fast moving trends. We reduce risk of loss by selecting trends with long lives and by staking out our positions in the early years.

e. Example: Solar’s rising share of the energy market driven by rapidly falling costs relative to fossil fuels.

f. Comments: Investing with the wind at your back stacks the odds in your favor to such an extent that we want roughly half our portfolios invested in powerful trends. By investing in the early years (the first third), we capture the bulk of the trend and reduce the role that timing plays in generating our returns. We dedicate more hours researching potential trends and identifying securities positioned to benefit from these trends than we spend on any other strategy bucket.

2. Washouts and Turnarounds:

a. Target Asset Allocation: 5% – 20% (for most portfolios).

b. Qualifications: First, the asset – usually a stock, sector or commodity – must have fallen 75% or more from its high point. We want road kill. Second, there has to be a valid reason to expect a recovery over the ensuing three years. We are looking for washed-out assets given up for dead, but that have unnoticed or under-appreciated change agents such as a new CEO, product or market niche. For companies, the balance sheet must be strong enough to give management enough time to execute a recovery plan without having to raise money in a highly dilutive manner.

c. Time Horizon: 3 year minimum for turnarounds. For cyclical washouts three years or an increase to at least 80% of the previous high.

d. Volatility/Risk: Volatile and risky but probably not as much as you would think because the huge price decline happened prior to our investment and the asset was already completely washed out of the weaker hands. Remaining shareholders are likely diehards. We can mitigate volatility and lower our effective cost basis by writing covered calls after quick increases in prices that may be followed by partial slide backs as it takes time for investors to change their perspective on the asset. Turnarounds are ideal candidates for this because their highly volatile past means their options are expensive.

e. Example: Blackberry has fallen 92% from its high point and has a new CEO focused on the enterprise market. Its call options also offer nice premiums; see item 4.e.

f. Comments: Studies demonstrate the impressive returns available over a three year holding period after an industries, sectors or countries has fallen by 70% or more. However, most company (especially technology) turnarounds never turn, so it is best to own numerous turnaround candidates because many will not recover so your profit will come from just a few holdings. Roughly speaking, the 80/20 rule probably applies where 80% of your profit comes from 20% of your investments.

3. Time Decay:

a. Target Asset Allocation: 5% – 15% (for most portfolios).

b. Qualifications: The asset must be structurally flawed and have a history of consistent deterioration. Two assets or tactics are available to us under this strategy:

i. Writing Put Options: Certain options have a high probability of expiring worthless. By writing (selling) OTM put options due to expire in less than 90 days we can consistently earn premiums (income). The key is to only do this on assets that we would like to own especially at a price below the current market value.

ii. Volatility Products: Certain ETFs try to mirror the vix index (a measure of implied volatility or fear in the stock market) but suffer massive decay from rolling over their futures contracts at unfavorable prices. 85% of the time they sell contracts which are about to expire at a low price then buy new contracts at a significantly higher price. This structural flaw is built-in to the term structure of vix futures and there are conservative way for us to benefit from this.

c. Time Horizon: Short-term (a few months) for writing puts because they expire quickly. Mid-term for volatility products which should be held longer to allow the compounding effect of roll-decay to build.

d. Volatility/Risk: Low volatile for writing puts. Medium-high volatility for vix products. Both strategies work best in a mildly falling, flat, choppy or rising stock market but are vulnerable to sudden market shocks. They don’t work during a steep stock market sell-off so they need to be modest in size and closely monitored.

e. Example: ZIV only corrects when fear is rising but otherwise generally appreciates in all other market conditions because it benefits from roll decay by doing the opposite of the volatility products mentioned above, in section 3.b.ii.

f. Comments: These are two methods for us to benefit from products that consistently decay over time. They nicely complements our other investments which generally require us to identify undervalued assets.

4. Income:

a. Target Asset Allocation: 10% – 25% (for most portfolios).

b. Qualifications: The asset must be safe. No point in taking on price risk with such limited upside especially for bonds where interest income is modest at best. Dividend paying stocks must be very cheap to minimize risk of loss from market declines. For these reasons we are currently under-invested in this strategy. Three tactics are available to us under the income bucket.

i. Buying Bonds: Investment grade corporate bonds, Treasuries and sovereign bonds provide modest interest income with low risk of loss provided they are held to maturity. A rise in interest rates rise would cause bond prices to decline and could easily negate interest earned. Directly owning bonds is superior to owning bond funds because funds charge fees but more importantly they never hold their bonds to maturity.

ii. Buying Dividend-Paying Stocks: The Fed’s low rates have already pushed fixed-income investors into dividend paying stocks, thereby elevating stock prices and reducing dividend yields. Reaching for yield in the stock market is a classic mistake but there will always be opportunities in some inexpensive dividend paying stocks with strong cash flow as well as some REITs and MLPs. For the time being, the pickings are slim.

iii. Writing Covered Calls: Low rates and elevated stock valuations is the perfect environment for generating income by writing (selling) short-term covered calls at strike prices 10–15 percent above the current mark value. By giving someone the right over a short period of time (30–90 days) to buy an asset we hold at a price 10–15 percent higher we collect a premium (income) which we keep regardless of whether or not they exercise their option. Most of the time the call option will expire worthless, then we can repeat the process if we wish. This is such a conservative income generating strategy that it is permitted in IRA accounts.

c. Time Horizon: Short-term for writing covered calls because they expire in 30–60 days. Mid-term for buying bonds and dividend-paying stocks.

d. Volatility/Risk: Low volatile and low risk for writing covered calls and owning short-term bonds. Medium risk for owning loner-term bonds. High volatility and risk for owning dividend-paying stocks which are always vulnerable to a sell-off in equity markets.

e. Example: Sell Blackberry April, $11 Calls for $0.63 with BBRY’s stock now trading at $9.82. If BBRY’s stock is not above $11 on 4/19/14 (12% appreciation in 52 days) the option expires worthless and we earn $0.63 on our $9.82 stock or 6.4% in 52 days from writing that call option. If BBRY’s stock is worth more than $11 on 4/19/14 we still earn $0.63 or 6.4% on the option but we also get the 12% stock appreciation from $9.82 to $11 for a total gain of 18.4%. Any appreciation beyond $11.63 (18.4%) goes to the option holder, not us. That’s what we give up for the sure thing of booking 6.4% in income every two months.

f. Comments: In our current environment of low interest rates and high stock prices in developed markets, tactic 4.b.iii. above – writing covered calls – is the safest way to generate income (premium) for our portfolios – it also happens to be the tactic that can generate the most income. Writing covered calls does not require the use of any capital (buying power) because the potential liability (owing shares if the calls get exercised) is fully ‘covered’ since the underlying asset is held in the account. Furthermore, a sharp stock market drop would accelerate the realization of income (premium) derived from writing covered calls. What we give up in return for these benefits is potential appreciation in the underlying asset above a preset price (the strike price) that I generally set 10 – 15 percent higher than the current market value. The majority of the time, this is a very good trade off.

5. Crisis Protection:

a. Target Asset Allocation: 5% – 15% (for most portfolios).

b. Qualifications: The asset must respond well to economic, financial and currency threats. If it generates profits when fear is rising then we want to own it to partially offset anticipated declines in our core holdings triggered by falling markets. Every portfolio should have some assets that make money during a crisis. There are three assets or tactics we use for protection.

i. Holding Cash: Obviously cash is king during a market correction however two issues limit its usefulness. First, it does not appreciate so you need to hold more of it for the same level of protection available with other products. Second, it loses value during a currency crisis mitigating its utility… but it does the job most of the time so we carry some. We consider short-term treasuries as cash equivalents.

ii. Inverse Stock Funds: These offer the best protection during economic and stock market weakness because they rise in proportion to how much equities decline. They work with minimal tracking error so we use them but at low levels because corrections cannot be timed well.

iii. Gold ETFs: Gold performs inconsistently during crisis. In the beginning of the 2008 financial crisis gold prices sold off along with equities but then rebounded sooner. Gold offers good protection during a currency crisis and high inflation. Further, gold historically does best during periods of low real interest rates, i.e., when interest rates are below or close to the inflation rate. We are in such a period today so we are holding some gold ETFs.

c. Time Horizon: Long-term because some level of protection (insurance) should always be maintained. The mix between the above three assets will change according to market conditions.

d. Volatility/Risk: Medium volatility but low risk because these assets are stabilizers for the overall portfolio. Like any property insurance, you don’t ever want to get paid since that means something bad has happened… and something bad always happens in finance.

e. Example: SH is an inverse stock fund that proportionally returns -1x the return of the S&P 500 stock index, with minimal tracking error.

f. Comments: Insurance is vital, but for a given time-horizon, you don’t need as much if you are diversified by asset class and strategy.

To summarize: By pursuing multiple investment strategies we further mitigate risk of loss while giving us more ways to win.

——–

Our Core Values As Investors

Mark’s ideas about following strong macro trends, targeting washouts (blood in the streets), income and diversification, and crisis protection are all core values we share with him as investors.

Taking note of the suggestions made above can help you achieve superior returns over the long run and trade or invest with a lot more confidence.

– Chris

“The only investors who shouldn’t diversify are those who are right 100% of the time.” – Sir John Templeton

Chris has founded and built several multi-million dollar businesses in the investment arena including overseeing the deployment of over $30m into Venture Capital opportunities and advising family offices internationally. Prior to this, Chris built a career at Invesco Asset Management, Lehman Brothers, JPMChase, & Robert Flemings.

This Post Has One Comment

I’d be interested to see how this ultimately pans out within the traditional asset class framework.