Three examples, one common thread. See if you can spot it.

Example 1: Dot-com

I remember the dot-com era.

Not because I knew what was taking place. Hell, I was not much past my teens and still cutting my teeth in the investment banking world, so I didn’t fully grasp the significance until years later.

But luckily for me it proved to be a baptism by fire in the dynamics of a spectacular boom. I recall marveling at the vast amounts of money being made.

- By the banks I worked for,

- By the companies being financed, and

- By the investors who bought into the companies, only to see their holdings rise in an almost uninterrupted fashion.

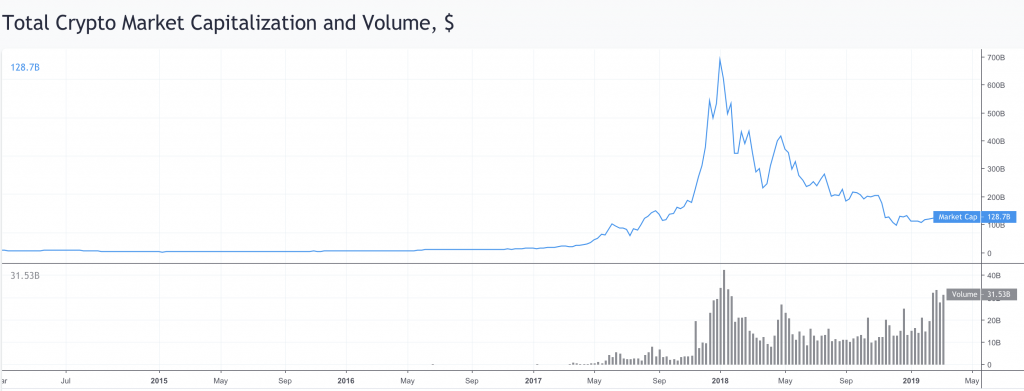

Example 2: Crypto

We all lived through this one. Some of the fastest money made on earth. Ever.

Example 3: Venture Capital & Private Equity

And now, for the boom that’s yet to bust.

Silicon Valley startups have been able to raise tens of millions of dollars with not much more than a couple of 20 somethings hashing together an idea and showing hockey-stick-like growth projections.

In terms of those they’re wishing to emulate, we have Google, Facebook, and let’s not forget the poster child of hogwosh accounting, Alibaba (Alibaba ain’t worth even half of what the market thinks it is).

The Connective Tissue

The connective tissue in all of these sectors is what I call “the unknown element”.

When the dot-com boom was just gearing up for its wild party, there were some outrageous stories that began to get told. This was while the champagne was still being sipped and partygoers were just getting tipsy. It took a few of those stories being believed (no matter how outrageous) before the partygoers now joined by many more said, “Well, look over here,” where company X just raised at Y valuation, then surely this can be justified elsewhere.”

And so in the end, everyone drank so much they couldn’t remember their names.

The crypto boom was not unlike the dot-com boom.

A new technology where nobody had seen it before, and so how big could it be? Nobody knew. And since this one is still fresh, the fact is we still don’t know, though I believe it’ll not be dissimilar to the internet, but that’s going to take time.

Moving onto venture capital and Silicon Valley tech in particular, you’re really dealing with massive unknowns. New technologies, new untested management teams and founders, and entire industry now built to facilitate it all.

In every business we can argue over whether or not 30% margins are realistic… or if they should be 25%. And we can argue over whether a company can grow at current annualised CAGR of 10% or is it likely to be closer to 8%.

Analysts will argue until they’re blue in the face over such things but at the end of the day these variables change the end result… but not by all that much. And importantly, they’re pretty boring for most people.

What really changes the end result and valuation is the unknown.

New technologies lend themselves particularly well to this. How the hell could an analyst in the late 80’s or early 90’s have figured out what e-commerce would look like in the future? He couldn’t.

How big could the market be? He didn’t know. How fantastic could it all be and what about that “early mover” startup with the CEO who wears a hoodie? Suck your thumb and try sound intelligent. That unknown element lends itself particularly well to bullshitting.

Takeaways

Two takeaways for you today.

Firstly, I can’t think of a sector more prone to bullshit optimistic assumptions and narratives than the natural resource sector.

- How big could the resource be Mr. CEO? Well, it COULD be huge. Massive, actually.

- How long can the deficit last? Well, forever (peak oil).

- We’ve a monstrous land package (probably worthless moose pasture), one of the largest in the whole of ___________ (insert area) and our preliminary analysis (we sucked our thumb) is that it could host the next elephant discovery.

Yes, folks it lends itself absolutely to “the unknown” and rest assured we’ll go through another cycle where the credulity of market participants will once again be tested and show us that human nature never changes.

It is why (if you’re signed up to this blog) you receive the Resource Insider podcast. It is why, after being bearish resources for years, last year we launched Resource Insider.

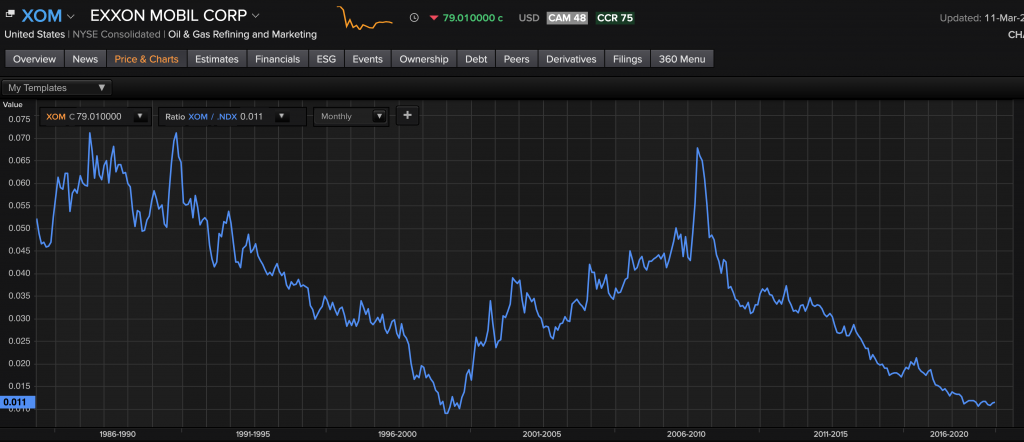

They say a chart paints a thousand words. Well, let it speak.

Here’s Exxon Mobil vs the NASDAQ:

And I could have picked half a dozen other companies or even the CRB index vs the NASDAQ and they’re all much the same.

The second takeaway has to do with the relationship between growth and value.

I’ve written fairly extensively about this before, but I’ll pretend you weren’t listening and so I’ll repeat it.

We’re experiencing a most extraordinary time where anything “growth” related has been bid to the moon and those good ol’ businesses which actually make money (value) have been treated like Harvey Weinstein at a woman against assholes rapists convention.

Take a look at the S&P Value Index vs the S&P Growth Index. Shunned!

We’d have to go back 20 years to find the same setup. Ain’t that something?

This has reached truly absurd levels as my buddy Kuppy recently pointed out in his excellent article on the topic.

Can it go on for longer? Sure it can, but if you’re anything like us, you look around at the partygoers and see that everyone is either stoned or drunk and they’ve not begun to realise that the booze is running low.

And you realise that at the same time there’s an extremely small and still rather subdued gathering (it’s not yet a party to be clear) taking place just down the road, where the cellar is stacked to the ceiling, the girls are all gorgeous, and there’s no competition because it’s only a handful of nerds wearing socks with their sandals sipping pensively on their tea.

This should be exciting to any investors who don’t just speak about being contrarian but actually look for deep value and act on it because the only reason nobody is going to this party right now is because they’re still enamoured with the wild party of yesteryear.

And since we humans are social creatures that move in flocks, everybody still wants to hang with the cool kids. And right now this party is not where the cool kids are hanging.

But ask yourself this. What exactly is the definition of asymmetry and which markets provide you with that today?

-Chris

“I like nonsense. It wakes up the brain cells.” — Dr. Seuss