As mentioned in my writing on the Singapore dollar, the most dangerous thing in finance is the “thing” that never moves. This stability creates an illusion of control around which many positions are built, the greater the perceived stability the greater the positions, and the more other assumptions and forecasts are made.

The stability (or lack of volatility) in the Renminbi has been the one of the foundations that has made so many other variables more forecastable. No one can imagine the Renminbi being a highly volatile currency, let alone coming remotely close to repeating what happened during the Asian Tiger crisis of 1997! If this foundation of stability suddenly disappears then there will be a great increase in uncertainty and volatility in many markets across the globe.

I don’t know exactly how a breakdown in the Renminbi will play out. However, it is a sure bet that all those markets that prospered over the last 15 years or so on the back of a China will do badly. Where things become shady is the collateral damage to other markets that have had nothing to do with the Chinese economic miracle.

I think a reasonable bearish position on the Renminbi will be a great way to hedge out the uncertainty of outcomes with respect to how the Chinese economic miracle “unwinds”.

For a long time I have been highly skeptical on the Chinese “economic miracle”. Every contrarian bone in my body has been telling me that there is something not quite right with China’s meteoric rise from an economy that was seemingly insignificant some 15 years ago to the economic powerhouse that we are led to believe it is today.

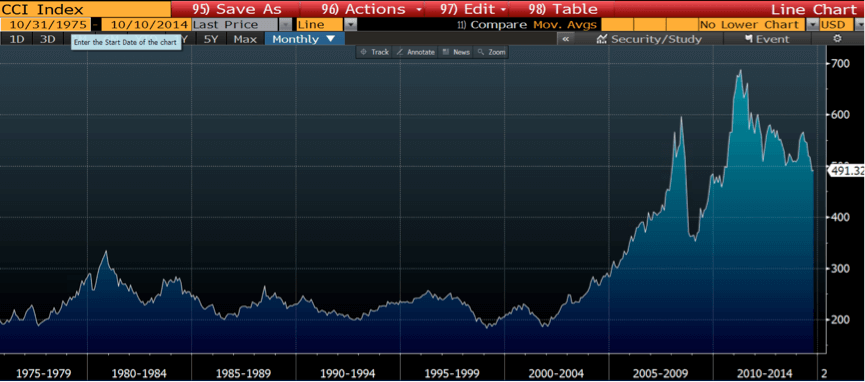

The Chinese economy has risen to prominence too quickly too soon. What has been the driver of this rise? Why did commodity prices explode skywards in 2002 having gone nowhere for the previous 30 years? I find it hard to believe that commodities became scarcer all of a sudden!

The CRB Commodity Index (the CCI)

The CRB Commodity Index (the CCI)

Well, no one has been able to give me a straight down the line answer – at least one that an ordinary average trader like myself could understand. That is until I came across the following discussion with Mark Hart. Hart came to prominence together with Kyle Bass after shorting the “sub-prime thing” in 2007.

Hart’s discussion on China starts at about the 55 minute mark. Note what Hart says about how he is applying his view on China (via options on the Renminbi). The interview was conducted in September but note that he has been “bearish” on China at least since 2011!

For more on the issues facing China you might like to read the writings of Gordon Chang and Michael Pettis. I think both present very objective views on China. I am not going to pretend to offer anything more than what these gentlemen offer with respect to the view on China.

Hart talks about buying “puts” on the Renminbi. What makes the trade so attractive is the extreme low level of volatility. Below is an index of implied volatility for 12 months to expiry at the money (ATM) calls on the USD/CNY.

So we can buy calls on the USD/Renminbi for about 2.5% volatility. For comparison purposes – implied volatility on the AUD/USD is about 10%!

Hart talks about buying the CNY 7 strike call on the USD/Renminbi. To give you an idea of the leverage offered on a 12-month option at the CNY 7 strike – about $1,100 will get you a notional position of $1,000,000! To achieve a payoff of 10x all the USD/CNY would have to close at is 7.07, and at 7.15 a 20x payoff is achieved!

One can now appreciate what Mark Hart is on about – the gearing offered by options on the Renminbi is huge because volatility is grossly underpriced.

Is it so crazy to think that the Renminbi can get to a “tick or two” above 7 within 12 months?

Well, let’s not forget what happened to currencies in the past. Note what happened to the Mexican Peso during the “Tequila” crisis:

…the Thai baht during the Asian Tiger crisis:

…or to the Russian Ruble during the LTCM crisis:

Currencies can move and they move significantly when they have been sailing in calm waters for extended periods of time – just like the Chinese Renminbi now. Position for the unexpected. It is why Hart and Bass made so much money during the Subprime crisis.

– Brad

“Never think that lack of variability is stability. Don’t confuse lack of volatility with stability, ever.” – Nassim Nicholas Taleb

This Post Has 25 Comments

on which markets are the CNY/USD options traded?

This is only traded on the Saxo platform to my knowledge. The code is USDCNH and you can go out 12 months. I would suggest allowing for a 5 year time horizon and allocating accordingly each year. Patience is required but the pay off is asymmetric which puts it into perspective.

Best of luck

Please kindly tell me what you think are some good alternative currencies to hedge against the falling Renminbi. HK Dollar? N

Another way to express a bearish view on the Renminbi is via the Singapore and Aussie dollars. If the Renminbi was to depreciate materially against the USD (USDCHY moves higher) then it would be due to the Chinese economy slowing more than expected which may also be associated with a credit crisis within the economy.

In any event I am sure that prior to any material depreciation in the Renminbi there would have already been material depreciations in the Aussie and Singapore dollars.

What would be my pick? The Singapore dollar. We can buy options on the USDSGD at half the price of options on the AUDUSD.

Any other ideas on where to execute this trade. Saxo Bank not available for US residents.

We can trade RMB futures on the CME here in the States, but they are very thinly traded:

http://www.cmegroup.com/trading/fx/emerging-market/usd-cnh.html

Options are those futures appear in IB but have zero prices.

I guess we can work with Brad’s suggestions here in the US.

I am told that Oanda http://www.oanda.com quote on the Renminbi spot market (no options).

good stuff… I checked the saxo platform and a 1m$ position for 12 months currently costs around 2k$. Im assuming the volatility jumped? Where can I check the quotes for CNH volatility the way you showed in the article (2nd screen)?

thx

Hello Lukas, yes volatility has begun to move higher. The only place I know of to get an index of implied vol is from Bloomberg.