Regular readers will have been very well positioned to take advantage of what is happening in emerging markets and specifically currencies as we can see from the fairly dramatic chart below.

We’ve been positioning for a USD bull run for some time now. Back in October we made the call that the yuan looked like it was providing us an asymmetric payoff opportunities as volatility was extraordinarily low, meaning that the market was not anticipating either volatility and certainly not weakness in the yuan. Here is what Brad said.

As mentioned in my writing on the Singapore dollar, the most dangerous thing in finance is the “thing” that never moves. This stability creates an illusion of control around which many positions are built, the greater the perceived stability the greater the positions, and the more other assumptions and forecasts are made.

Then in November Brad mentioned that:

A bull market in the US Dollar is underway and its magnitude and duration are likely to catch everyone by surprise. I believe it isn’t out of the question for the USD Index to advance by at least 50% within the next 5 years. If this forecast proves correct, there will be profound ramifications for the global economy and many financial markets, particularly emerging markets.

Not to beat a dead horse earlier this month we detailed further reasons to get long USD and short yuan.

We believe this trade has some legs and though volatility is no longer as cheap as it was when Brad first began yelling from the rooftops we believe we’ve some ways to go in this yet.

Since we believe it’s of such importance over the coming 2015 year we’re putting the finishing touches to a comprehensive guide to profiting from this which we’ll be sending to subscribers. If you’re not already on our list make sure you’re on it.[mchimp_signup group=”Twice Weekly”]

With that prelude I wanted to share an article on recent events in Russia from our sister site Emerging Frontiers which covers the frontier and emerging markets.

————

Mayhem! Carnage! Каtасtрофа!

These are the messages that blared forth from my TV screen and broker notes this morning. Monday – hereafter branded as “Red Monday” – was a day of reckoning for the Russian economy. The schadenfreude on display in Western media is nearly as relentless as the ruble’s sell-off:

“It couldn’t happen to a nicer guy” — WSJ, on Putin

“Russian sanctions could be lifted ‘within days’ if Vladimir Putin makes different choices, John Kerry says” — Daily Telegraph

Let’s disregard the fact that Secretary Kerry may be a bit premature with the sanctimony after two years of diplomatic outmaneuvering and general поражении (beatings) at Putin’s hands in Syria, Libya, and Ukraine. It might be easy to get caught up in the media hype around yet another Russian currency crisis, but time can be better spent in considering what Putin’s next moves might be, and the ramifications for the global economy.

Few will disagree that Vladimir Putin is easily the most effective head of state on today’s world stage. Americans may not like him, but Russians love and adore him. Trust me on this one, Mr Putin is not going anywhere and the only effective outcome of Kerry’s sanctions has been to unite the Russian people in defense of their president.

Let’s quickly recap the facts as we know them now:

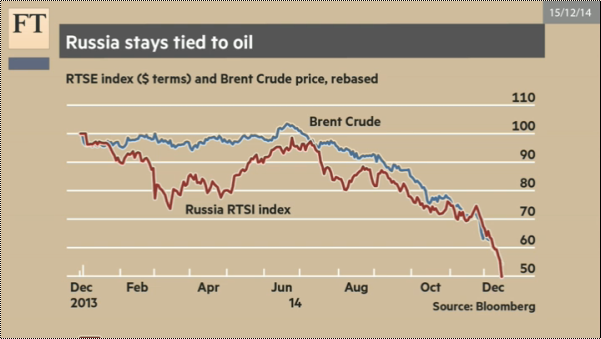

- Crude prices are at a five-year low; WTI traded below $57, and Brent just passed through $60 for the first time since 2009.

- On Monday the ruble (RUB) dropped nearly 10% against the US Dollar (USD) in a single day of trading.

- In the early morning of Tuesday the Russian Central Bank (CBR) raised rates from 10.5% to 17% – a 62% increase in the overnight lending rate. This stopped the RUB’s downward slide – for less than two hours – before continuing down past the 75 handle.

- The RTS, Russia’s benchmark equity index, was down 12% on Tuesday when I wrote this and lost nearly 40% in the month of December.

Courtesy: Financial Times

Courtesy: Financial Times

All of this information is readily available – but what does this mean for the global markets? How can we predict the “second bounce of the ball” or the unintended consequences of the Russian implosion?

I lived and worked in Moscow for a couple of years, and during my tenure the RUB never breached the 32 handle. This morning a friend told me via email that middle-class Muscovites are piling into IKEA, 7th Continent and other large retailers to buy every consumer good on the shelves before the inevitable mark-ups are applied. I only wish that I were there to load up on deeply-discounted bottles of Kalashnikov vodka – a much better souvenir than the NFL-themed matryoshka dolls from the tourist traps at Ismailovskiy Park.

Russia’s first post-Soviet currency crisis, in 1998, pre-dates my arrival there but I often heard about how market traders would price their goods in “conditional units” instead of rubles – a thinly-veiled attempt to price their goods in USD (which is illegal; Russian businesses can only price their goods in RUB).

It is virtually indisputable that Russia will experience a painful recession next year; their economy’s most significant shortcoming is its near-total reliance on resource exports. Russia’s break-even production cost of crude oil is just over $100, so the country’s famed $400bn “stabilization fund” will soon begin to draw down. Russia has its problems, to be sure, but their fiscal policy has actually been quite solid since they launched this fund in 2004 to mitigate volatility in the crude oil market.

Let’s tick off some other, lesser-known (but no less true) facts:

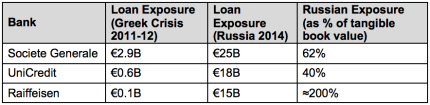

- Remember the European mega-banks that were imperiled in the Greek sovereign debt crisis of 2012? Disaster was only averted when ECB President Mario Draghi pledged to do “whatever it takes” to save the Euro? Let’s take a look at current exposure to Russia for some of the largest European banks (courtesy of Bloomberg). How much of this exposure was denominated in US Dollars? I suspect that we’ll soon find out. This week’s events will surely serve as a wake-up call for the sovereign debt markets – remember that, less than three months ago, Spain and Italy were pricing bond issuances at a lower yield than US Treasuries!

- Russia’s gold reserves are at a 20-year high now, with over 1,150 tons (worth over US$ 1.5B) on record. Theirs is the fifth-highest stockpile, having just passed China and Switzerland. Does the US hold more in Fort Knox? Good question! The Fed refuses any attempt to independently audit its reserves. Even if you’re not a “gold bug”, you have to appreciate the (image of) stability that these holdings can convey to the world in a full-on currency crisis.

- Russia has made no secret of its interest in dethroning the US Dollar as the global reserve currency. Recent moves such as the establishment of the New Development Bank (also known as the “BRICS Bank”), and joint efforts with China to begin direct currency conversion with their respective trading partners (and each other) are beginning to chip away at global dollar hegemony.

Make no mistake, this sell-off is a big problem – not just for Russia, or for the other over-levered emerging market currencies (TRY, INR, ZAR) that stand to be traumatized by a rising US dollar, but ultimately even for the US itself. As US capacity utilization returns to pre-2001 levels, and inflation gains momentum, dollar-pegged currencies around the world are about to come under increasing strain. I expect that Putin’s plans to chip away at the global reserve currency – the US Dollar – are about to shift into high gear.

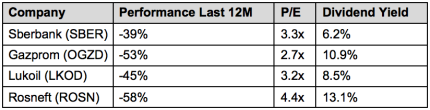

I’ll be watching this situation closely. In the meantime, some food for thought… it might be time for investors to give some serious thought to the major Russian names out there. Here is what I saw in the GDRs this morning…

Current prices, P/Es and dividend yields for Russian majors:

Of course one must remember that these companies’ ability to pay such attractive yields may be imperiled by crude prices that are currently 40% below Russia’s production break-even. Nonetheless, it’s indisputable that there are going to be some real bargains in this market. (Disclosure: I own all of the stocks on this list in my personal account. This is not a recommendation; make your own decisions please!)

I’ll write more about this in a few days. I’m increasingly of the opinion that 2015 is going to be a year that investors will someday tell their grandchildren about.

————

Certainly something to think about over the weekend which I hope you enjoy as much as I plan to. I’ll be enjoying some quiet time and staying well away from any retail outlets where people will be amassing in force trying desperately to figure out what to buy for people who don’t need anything and who in turn will be out doing the same thing, all the while maintaining the same fake enthusiasm for Christmas as North Koreans did for Jim Jong Il.

– Chris

“Under the most negative external economic scenario, this situation can last two years.” – Vladimir Putin on 18 December, 2014