Ten days ago China cut interest rates in an effort to free up credit and stimulate the economy. This is unlikely to have much of a positive effect on economic growth in China. Rather it is likely to compound the big problem that the Chinese currently face: exports becoming increasingly uncompetitive.

China’s biggest problem is its strong currency, the renminbi, caused by a strong USD. As the USD rises its exports become less competitive. What if currently cheap Chinese products on the shop shelves worldwide become less cheap and outright expensive as the USD continues down the path of a multi-year bull market. Cutting interest rates in China won’t have any affect on making Chinese exports more competitive.

I am not an economist. Rather I am a macro trader and I look for relationships in global financial markets on which to base my views and trades. There has been considerable talk about the Chinese economic miracle over the last few years, but I believe that much of that “miracle” or “economic growth” has occurred on the back of a weak USD and cheap credit. Note how Chinese GDP started to go parabolic from about 2002 onwards.

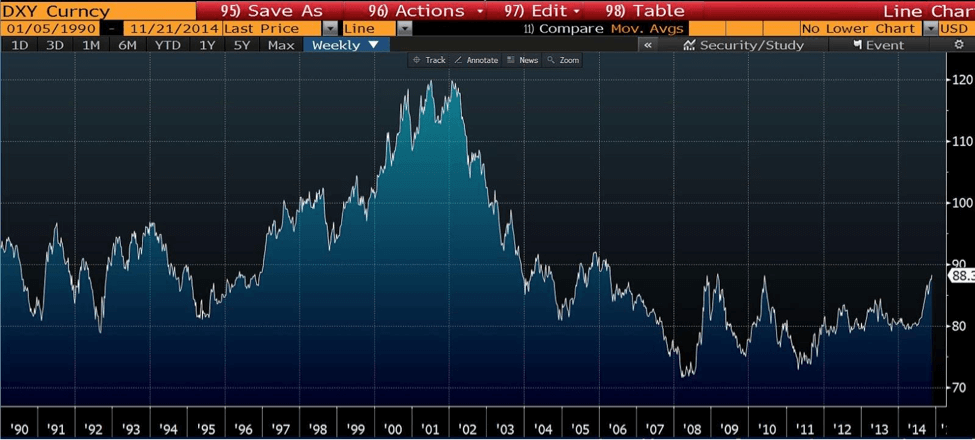

Also note how the USD (as per the US Dollar Index) went into a bear market at about that time:

Yes, this may be a little simplistic but – what if the USD continues to rise from here and it trades at a new high within 5 years (I’m trying to be conservative), and the renminbi doesn’t depreciate against the USD in any material sense? I don’t think it takes much to work out that the Chinese economy would be in a recession if that were to occur! Either way – if the USD continues to appreciate over the coming months then the renminbi has to depreciate!

So all we have to do is to get the direction of the USD right and everything else falls into place. I have talked at length about the USD on a previous occasion. Nothing has changed to my perspectives since then, so I won’t badger on about it here.

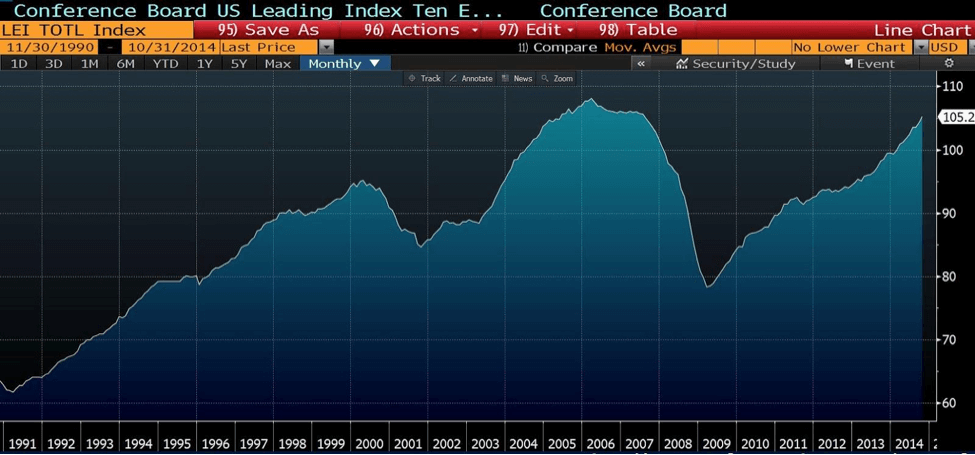

What about interest rates? If interest rates eventually track what is happening in the economy then to me it is just a question of when, not if rates will rise in the US. Given the behavior of leading indicators, interest rates in the US are likely to rise much sooner than is generally expected. The up trend of leading economic indicators doesn’t seem to be in any danger, rather momentum appears to be gaining to the upside.

While there is a lot of debate as to when interest rates will rise, there has been little debate as to the magnitude of rate rises. Below is the yield of the US 2 year treasury; it has been engaged in a relatively tight trading range for the last 4-5 years. Usually breakouts of sideways trading ranges are dramatic. So don’t be surprised to see rates move materially higher very quickly once the US 2 year yield breaks above 1%.

So we have a situation in the US where rates are getting ever so close to rising due to economic growth picking up, whereas rates are being cut in China due to economic activity slowing down. Combine this with a rising USD and it will certainly lead to a continuation of the unwind of the carry trade.

Charles Hugh Smith published a great article on the USD – “Why the Rising US Dollar Could destabilize the Global Financial System”. In the article he details the essence of the carry trade:

We might imagine that the Federal Reserve ending its vast money-issuance program of quantitative easing would lessen the global risk posed by the carry trade, as it reduces the flood of dollars seeking higher-yield homes outside the U.S.

But this tightening has actually increased the risk of carry trades blowing up and bringing down emerging-market economies, for it reduces the flow of fresh capital into emerging markets. As the supply of dollars dries up, demand for dollars rises as carry trades are unwound. Emerging-market currencies then weaken significantly, causing profitable carry trades to reverse into losing trades, which then causes those holding debt in dollars and assets in other currencies to dump the assets and pay off the dollar-denominated debts before the trade goes even more against them.

There is a positive feedback in play: the more the dollar rises, the greater the losses in carry trades denominated in the dollar, and the greater the incentive for those still in the trade to sell emerging market assets and currencies.

In response to these massive outflows of capital, emerging nations must raise interest rates quickly to offer incentives for capital to stay put, which then causes the cost of new loans (and doing business in general) to quickly rise to painful levels.

Although the renminbi isn’t depreciating against the USD, cutting rates in China does reduce the attractiveness of the Chinese carry trade. If the renminbi did start to depreciate against the US dollar then it would likely depreciate very quickly given the amount of capital that is locked up in the Chinese carry trade. This would lead to massive inflationary pressures that would eventually force the PBOC to raise rates to defend the currency (in so doing killing economic growth) and then we have a fully-fledged renminbi crisis on our hands.

Perhaps this is what the Chinese authorities fear, but it is what ultimately will happen if the US dollar continues its upward trajectory. The crowd has placed a very low probability of this situation playing out which is why we have begun a program of buying extremely cheap long dated call options on the USD/renminbi. Now we sit back and watch the slow motion train wreck begin to unfold.

– Brad

“Let China sleep, for when she awakes, she will shake the world.” – Napoleon Bonaparte

PS: Whether you’re an individual investor looking for high-quality research and information to help steer through increasingly treacherous markets, or an investment professional looking to provide clients with solid, expert analysis and ideas to do the same thing, this report on global debt will interest you.

This Post Has 4 Comments

With all due respect and best wishes on your trade…

A lot of false facts here and false conclusions. First the rate cut if you carefully read the PBOC original release and not just headlines, is accompanied by 1.2 instead of 1.1 times “band” for the bank, so actually banks can pay more not less for deposits following the “cut” … up to 3.3% instead of 3.25% .. so there is no real life rate cut.

Second, the all thesis of strong USD = Uncompetitive Chinese exports, is false, you have to understand that competitive has many factors, currency is only one of them, labor is second, energy is third, efficiency and infrastructure are factor as well, a good example which put this thesis to sleep, is Hong Kong, Hong Kong pegged to the dollar since 1983 at 7.75HKD:$1 ,Looking at HK exports to the U.S. in periods of strong USD , there is no weakness and still a strong uptrend, there is organic growth, value in the infrastructure etc… it is not currency only… talk to a buyer at wall mart importing from China, see if they will import from Thailand same product if they were not sure as to delivery time , ability to execute the quantity and other factors such as credit etc….. it is not that simple… HK example is a good lesson how things are not that simple and how strong USD does not necessarily mean bad or good for that matter to exports.

There is also a difference between correlation and causation, saying China boom started when USD started to weaken around 2000, but forgetting to realize that that is actually when China joined the WTO is a mix of correlation and causation…

The Yuan can weaken but the reasonings given are plain false, (like a guy with six pack eating potato chips can not say potato chips lead to six pack) I think each and one of the factors mentioned does not hold any test in reality if one look at facts and put opinions aside, that included the carry trade size compare to country reserves etc…

I have no issue about speculating on opinions, my issue is having opinion and then dressing it as fact which is clearly false

Thanks so much for the thoughtful critique.

You mention Hong Kong as an example but I think the HKD and Hong Kong situation is a unique one and not fully understood.

As I’m sure you are aware, ever since the peg was put in place any number of economists, commentators and speculators have had their say on the HK Dollar.

The fact is as long as the HKMA is committed to the peg they can defend it ad infinitum. I say this because people have tried many times to speculate against the currency because of its “flaws” but have always failed. Three banks issue notes in HK. HSBC and SCB and originally Mercantile Bank which was taken over by HSBC years back but the licence was never killed off and when PRC took over HK, BOCHK became a note issuer, a fact of some significance I would say! Actually I recall it was before the actual Handover. HK has US$ 325 Bn of foreign exchange reserves enough to kill of all comers. I must say I had thought that maybe when the HK$ and RMB reached parity that the mainland and HK might merge their currencies but that never happened and the RMB went sailing on. HK as an economy has long got used to the issues associated with the HK$ peg against the US$ and don’t seem to have done too badly. So, housing has run away into the realms of insanity but then again some people believe that London has done the same. There is of course more to this including debt financing costs in the western markets, perpetuated by “wise” central bankers acting benevolently. Of course HK will always have a supply problem due to it’s geography. Property bubbles, like stock market bubbles, do correct eventually but sometimes you have to hang on to your principle belief a lot longer than common sense would suggest and nowadays the so called “long term horizon” has got shorter and shorter, even to the next day!

Anyway as long as the HK$ exists as a currency I would say that the peg will exist too. It is hard to imagine a circumstance where the HKMA would abandon it after it has served them so well for so long.

At the end of the day the HKD is not the Yuan…not yet anyway and can’t and shouldn’t be used as an example here any more than the Zimbabwean dollar could be used as a proxy for the South African Rand. There are strong similarities BTW with that analogy but I’ll leave that for another day.

HKD from 1983 to 1985 before we had the hindsight bias that the HKMA will defend the peg the way it did, the USD moved from 120 to 160, same time HK exports moved from 15 to 25 million, in the 90’s prior to 1997 handover same thing USD up exports also up….Singapore dollar in the 90’s during strong dollar times, exports up and currency up huge together as well. I am sure we can go all day find example in both directions which lead to my point that things are not black and white as in your post, there are lot of factors involved and saying strong USD= this or equal that is simply a total misunderstanding of how the world works, the rest of the world does not remain static, China does not remain static. Also, having opinion and THEN looking for data points to explain it, is very dangerous, that is how one misses that it might actually be China joining the WTO that caused the boom staring in 2000 not the USD…

No matter you are a big investor or small everybody needs is accuracy in the calls on which they are trading. So one should go for the best trading advisory firm to get good amount of returns.