With over $900 billion invested into bond funds by mom-and-pop investors since the global financial crisis, the great law of unintended consequence is gearing up to rear its ugly head. Once again, money will be taken from those least able to afford it.

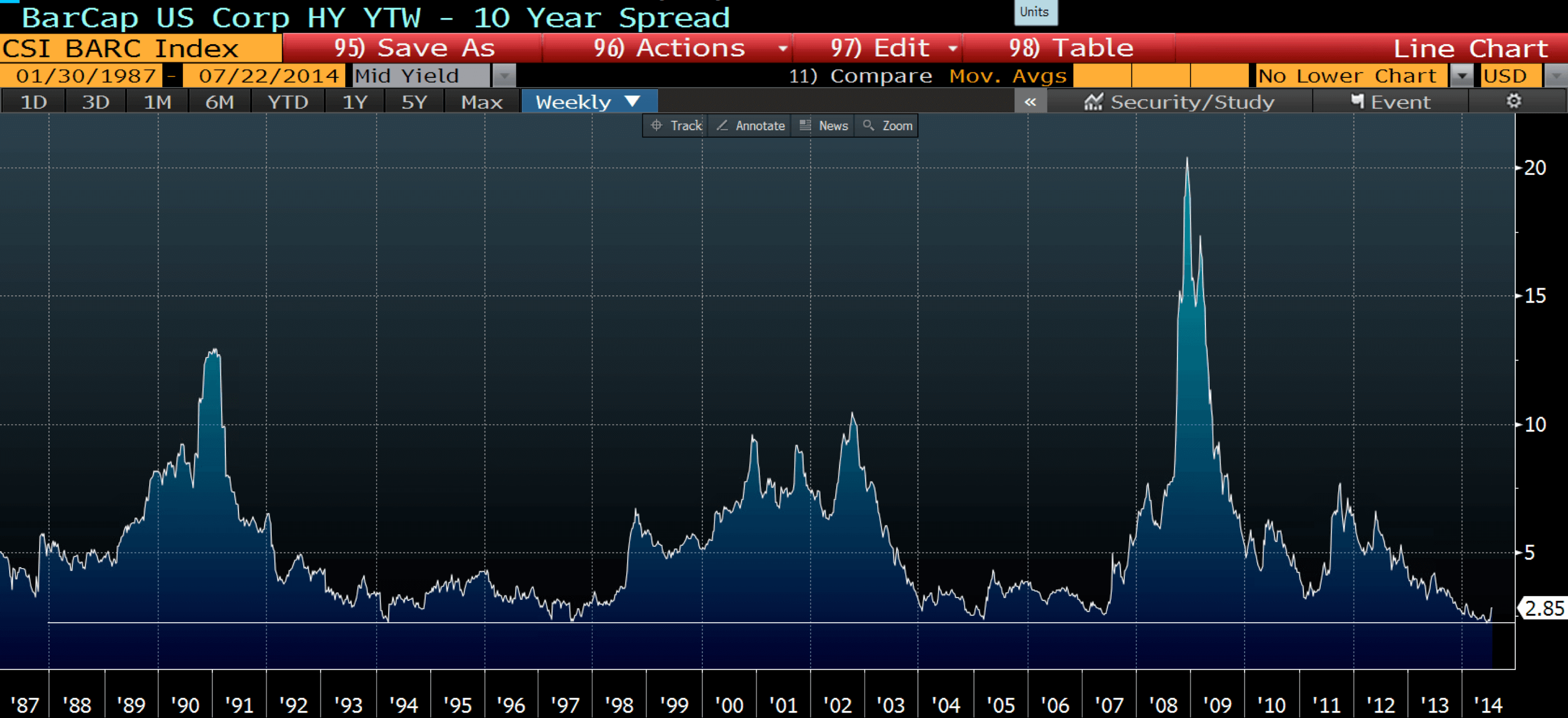

Take a look at the graph below, which shows the spread between junk grade bonds and US treasuries (the 10 year). You’ll note how the spread isn’t really a “spread” anymore because it has been squeezed to almost zero by delusional, yield-hungry fools. A premium of some 2.5% above the US 10 year treasury is nothing short of insane.

This is indicative of how crowded the bond market really is. Thank you central bankers for your service to mankind.

“Relative value” is increasingly what investors seek, in the process of leaving common sense on the breakfast table. As our monetary overlords punish savers, those savers turn to other “relative” yield investments to obtain interest rates over and above that which is offered in the completely pathetic government debt markets.

Naturally this has led them into junk bonds. Ask your neighbour if he knows what a junk bond is and he’ll likely stare blankly at you. Ask him where he’s investing and he’ll quite possibly tell you “high yield bond funds”. Safety is important you know. Bonds are safe. Much safer than equities. Really?

Consider that debt rated below Baa3 by Moody’s and lower than BBB by S&P has declined to 5.96%. To put this into perspective, the average yield over the last decade for these bonds is 8.91%. A return to the mean is sure gonna hurt.

Now let us play devil’s advocate for a minute. What if central bankers follow through with their threats to reign in stimulus? I know, I know they’ve painted themselves into a corner but let’s play the game, shall we. Should they follow through there would be an exodus out of bond funds, causing credit markets to freeze up.

The real question to ask ourselves is this. What if the market decides to begin acting ahead of, or despite the actions of central bankers. In most instances of dramatic crisis market forces drive values and price moves not central bankers, who typically rush in to “save” the situation after the fact.

Now imagine the effect on junk bonds which are less liquid than say treasuries, should the market begin to react to severe miss-pricing of risk, or indeed QE takes a walk over the horizon and does not return. As interest rates tick higher it’s not hard to imagine some of these bonds going no bid for long enough to cause a few heart failures. In a crisis some of these overleveraged companies sitting in fund managers portfolios will not be able to refinance their debt and for bond holders it may well be a 100% wipe-out. There is a reason it’s called junk.

There are a number of ways to position for sanity to return. Directly shorting via futures, buying puts on junk grade bonds or even junk bond ETFs. Instead of pinpointing one or two, feel free to look at any of these, which is a list of junk bond funds.

Asymmetric trading opportunities like the one just discussed are the brainchild of Brad Thomas, not me. The trades he and I discuss and write about herein are indicative of the sort of positions he takes in his fund, which is currently closed to new investment. Please drop your email in the box below and we’ll notify you when it is taking investment and you’ll be provided with additional information.

[mchimp_signup group=”Brad Fund” title=”Brad Thomas’ Investment Fund”]

We share these ideas with you so that hopefully investors who are long might at least consider the setup and act in accordance with that knowledge. Even if Brad is wrong, the return or compensation for taking on such risk is just mind-blowing. Caveat emptor.

– Chris

“The past is always triple-A. We can all remember what the past was. But if we try to make the future triple-A, we have no future. The future is always single-B.” – Michael Milken

This Post Has One Comment

Where can you trade futures on high yield bonds?