Market dislocations occur when financial markets, operating under stressful conditions, experience large widespread asset mispricing.

Welcome to this week’s edition of “World Out Of Whack” where every Wednesday we take time out of our day to laugh, poke fun at and present to you absurdity in global financial markets in all its glorious insanity.

While we enjoy a good laugh, the truth is that the first step to protecting ourselves from losses is to protect ourselves from ignorance. Think of the “World Out Of Whack” as your double thick armour plated side impact protection system in a financial world littered with drunk drivers.

Selfishly we also know that the biggest (and often the fastest) returns come from asymmetric market moves. But, in order to identify these moves we must first identify where they live.

Occasionally we find opportunities where we can buy (or sell) assets for mere cents on the dollar – because, after all, we are capitalists.

In this week’s edition of the WOW: An Absurd Unintended Consequence Of Abnormally Low Interest Rates

Even the dullest amongst us have heard about compound interest.

The story goes like this: you can become wealthy – not rich, but wealthy – by foregoing those lattes, $100 haircuts, and saving a decent portion of your income. You earn interest on those savings and let it compound.

By the time your hips are giving in and your bladder has begun to leak it’s all turned into a decent little stash while the Jones’ next door who’ve spent their lives upgrading the Lexus every year and holidaying in Hawaii will be asking you for a loan to pay for the leaking roof.

This all works when you can actually earn interest on your money.

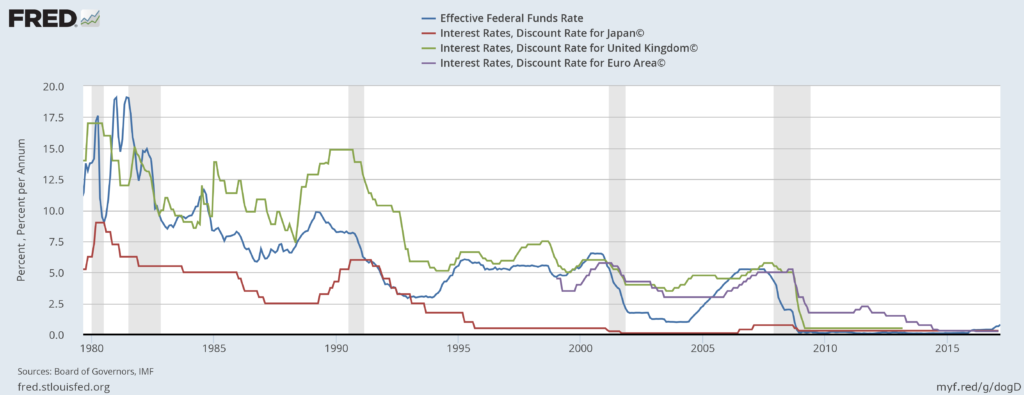

And so ever since our central bank overlords with their well intentioned but entirely destructive policies have driven rates through the floor the ability to achieve yield has been destroyed.

The distortions globally are truly breathtaking.

Take a look at this:

In the world of illiquid private assets such as venture capital and private equity asset prices are determined largely by:

- The valuation based on the last successful financing round

- Any liquidity event (trade sales, IPOs)

- Or… “belly-upedness”

Last month the WSJ ran an article about Investindustrial, a European private equity fund run by one Andrea Bonomi who, while running an existing fund, just raised gobs of new money ($800m to be exact) and launched a new fund to buy the assets of the old fund.

Wait! What??

![]()

The story, according to the WSJ, goes like this:

“Buyout firms face increasing competition from patient investors like sovereign-wealth funds. One has found a way to play them at their own game: Investindustrial, a European buyout firm, is creating a new fund to buy €750 million ($800 million) of assets it already owns.

Investindustrial, founded by Italian dealmaker Andrea Bonomi, has decided on this novel course of action as it responds to greater competition for assets from institutions such as sovereign-wealth funds, which don’t have restrictions on how long they can own companies. The competition is pressuring buyout firms to devise new ways to own companies.”

Maybe…

Let’s put ourselves in the shoes of Bonomi and ask a few of questions.

How would you solve a “valuation issue” as well as a “liquidity issue” when, after looking for buyers for your funds’ assets, the intersection of willing buyer and that of your private equity fund’s NAV doesn’t intersect where it “should”?

If you could turn fictional paper profits into real ones with a liquidity event, would you?

If you could earn fees on both the buy and sell side of a transaction, any transaction, would you?

If you couldn’t find a buyer at the valuations you’ve been reporting to your LPs, pray tell, how would you solve both the “valuation” and “liquidity” problem?

Looks to me like Andrea is taking the mickey, but hey, if he can find fools investors willing to go along with it then who am I to be a buzz kill?

Tip of an iceberg…

Now consider pension funds who, in order to maintain their funding, need to deliver a particular return. Returns, I might add, which the liquid market are quite simply not providing them.

Remember, pension funds invest the vast majority in “safe” investments and are therefore predominately invested in fixed income markets, which brings me all the way back to the chart I started this discussion with. Yikes!

As you can see by going to zero or negative interest rates, the true market price of risk isn’t just distorted, it’s largely completely unknown at this point.

Since the market can’t function through proper price discovery mechanics quite literally every asset price globally – whether it be equities, bonds, real estate, and even cash – is distorted.

Ask any money manager what method they’re using to price risk premiums at and they’re all lost. Nobody really knows and yet we have to price assets somehow.

Private equity assets, for their part, provide these guys with an ability to extend maturities and on the face of it reduce volatility. After all, how volatile is an asset which only changes hands once every 5 to 10 years and one which has done nothing but go up as investors have been pushed further and further down the risk curve?

As Bloomberg recently pointed out:

“According to The Pew Charitable Trusts, allocations to alts by pension funds have gone from just 11 percent in 2006 to almost 30 percent today.”

And as Credit Suisse in a research note mention:

“In 1980, there were only 24 private equity firms and deal volume only modestly exceeded $1 billion. Today, there are more than 3,000 U.S. private equity firms and assets under management for buyout funds are roughly $825 billion, up from $80 billion in 1996 and less than $1 billion in 1976.12 Two of the largest private equity firms, The Carlyle Group and KKR & Co, each have more than 720,000 employees in their portfolio companies, which means they both employ more people than any U.S. listed company except for Wal-Mart Stores, Inc.”

Private equity ticks many of the required boxes for pension funds.

- Reduced volatility (until you have to sell),

- Higher returns.

And that, my friends, opens a whole new can of worms because, as the demographic pig moves through the python, redemptions will increase, meaning asset sales will need to be taking place. And this right at a time when global liquidity is contracting. But that is a fun topic for another edition of World Out Of Whack.

Question for the day

“Low and expanding risk premiums are at the root of nearly every abrupt market loss.” — Raghuram Rajan, the governor of the Reserve Bank of India, who is one of the few economists who foresaw the financial crisis