Market dislocations occur when financial markets, operating under stressful conditions, experience large widespread asset mispricing.

Welcome to this week’s edition of “World Out Of Whack” where every Wednesday we take time out of our day to laugh, poke fun at and present to you absurdity in global financial markets in all its glorious insanity.

While we enjoy a good laugh, the truth is that the first step to protecting ourselves from losses is to protect ourselves from ignorance. Think of the “World Out Of Whack” as your double thick armour plated side impact protection system in a financial world littered with drunk drivers.

Selfishly we also know that the biggest (and often the fastest) returns come from asymmetric market moves. But, in order to identify these moves we must first identify where they live.

Occasionally we find opportunities where we can buy (or sell) assets for mere cents on the dollar – because, after all, we are capitalists.

In this week’s edition of the WOW: global real estate

Ever since anyone can remember, global real estate prices have been going up. Pretty much doesn’t matter which country you’re from (unless, of course, it’s Syria, or Iraq… or Fuhggedistan): if you bought something in the last 2 to 3 decades, it’s like the ceilings were insulated with helium. Even when the 2008 crisis hit and we had Captain Clever ensuring the world that things were just peachy:

“At this juncture, however, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained. In particular, mortgages to prime borrowers and fixed-rate mortgages to all classes of borrowers continue to perform well, with low rates of delinquency.” – Ben Bernanke, March 28, 2007

Even with that setback real estate has marched upward. The US, of course, took a decent breather and is only today back to where it was pre the GFC.

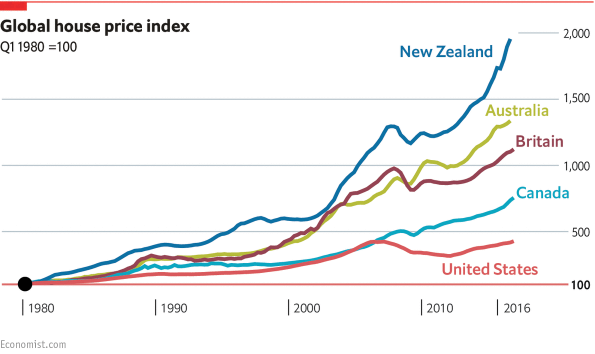

But the US isn’t the world, so let’s look at what everyone else has been up to.

Take a look at this:

In the British empire and all its former colonies the inmates pretty much trucked on after a short “uh-oh” moment:

“Did you see that Bobby? Blimmin Mary reckons the place down on the corner only fetched a million quid.”

“Musta been a steal laddie, it even had a fence. Reckon we ought to get out and buy already.”

And so they did as we can see.

In truth, it hasn’t just been Mr. and Mrs. Smith in their tweed coats buying up UK properties, just as it hasn’t been Sheila and Bruce in Sydney, or even Maple and Hudson in Canada. A significant amount of buying power in these markets has come from offshore buyers, largely frightened Chinese money being parked. It’s pretty extraordinary, really.

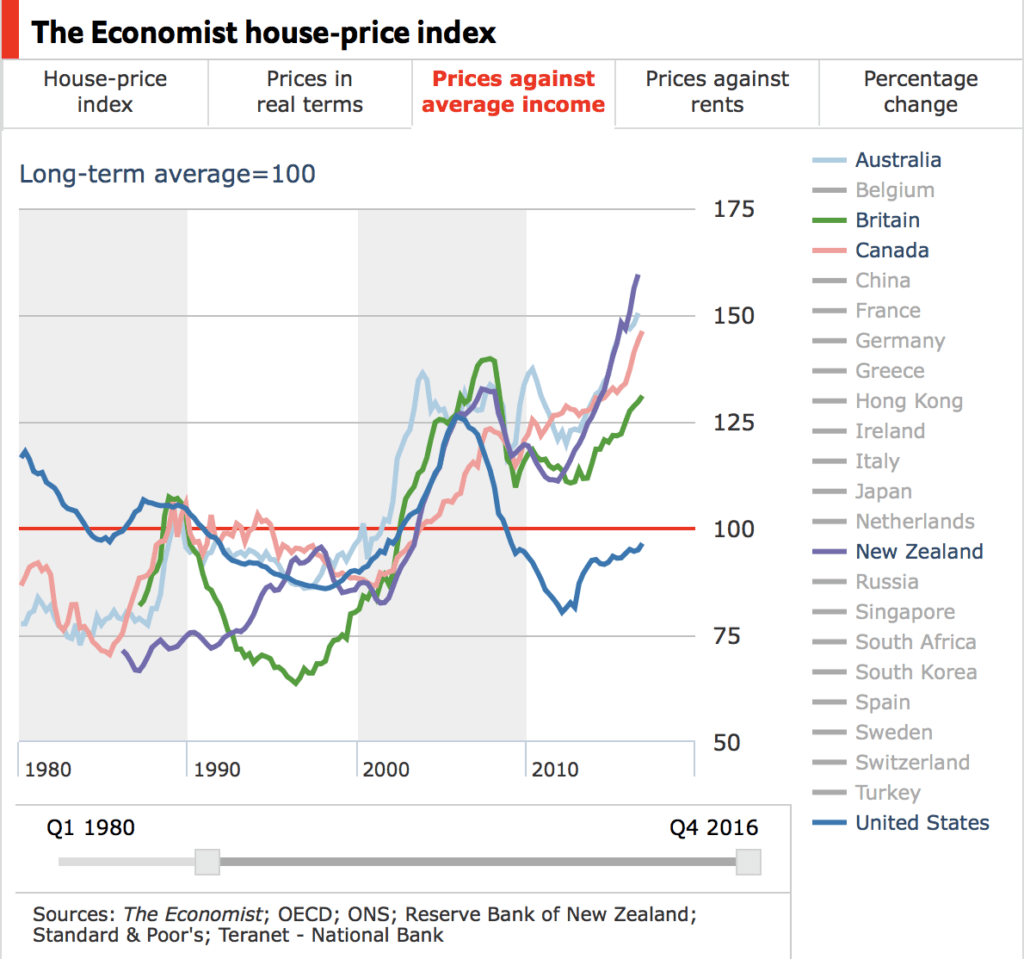

Prices alone don’t provide us with the entire picture or provide us with context. I mean, real estate prices in Harare went through the roof, too, in the 2008-09 period (in ZWD) but the currency went through the floor and real purchasing power collapsed. Context, therefore, is important.

Also, clearly a swanky penthouse in Manhattan overlooking the Hudson river shouldn’t be priced the same as a swanky penthouse in Vientiane overlooking the Mekong. The main difference? Incomes.

So let’s take a look at prices relative to incomes for a better understanding.

Buying a house in the US actually makes a lot more sense. Certainly relative to its international peers the US is cheap. In fact, if you factor in the ability to fix debt for a ridiculously long time in a currency that’s ultimately going to get hammered, and if you need to find somewhere to live then you’ve found a way to essentially be synthetically short the bond market (provided you fix your rates). I’m not advocating this as a strategy but merely pointing out the mechanics of the trade.

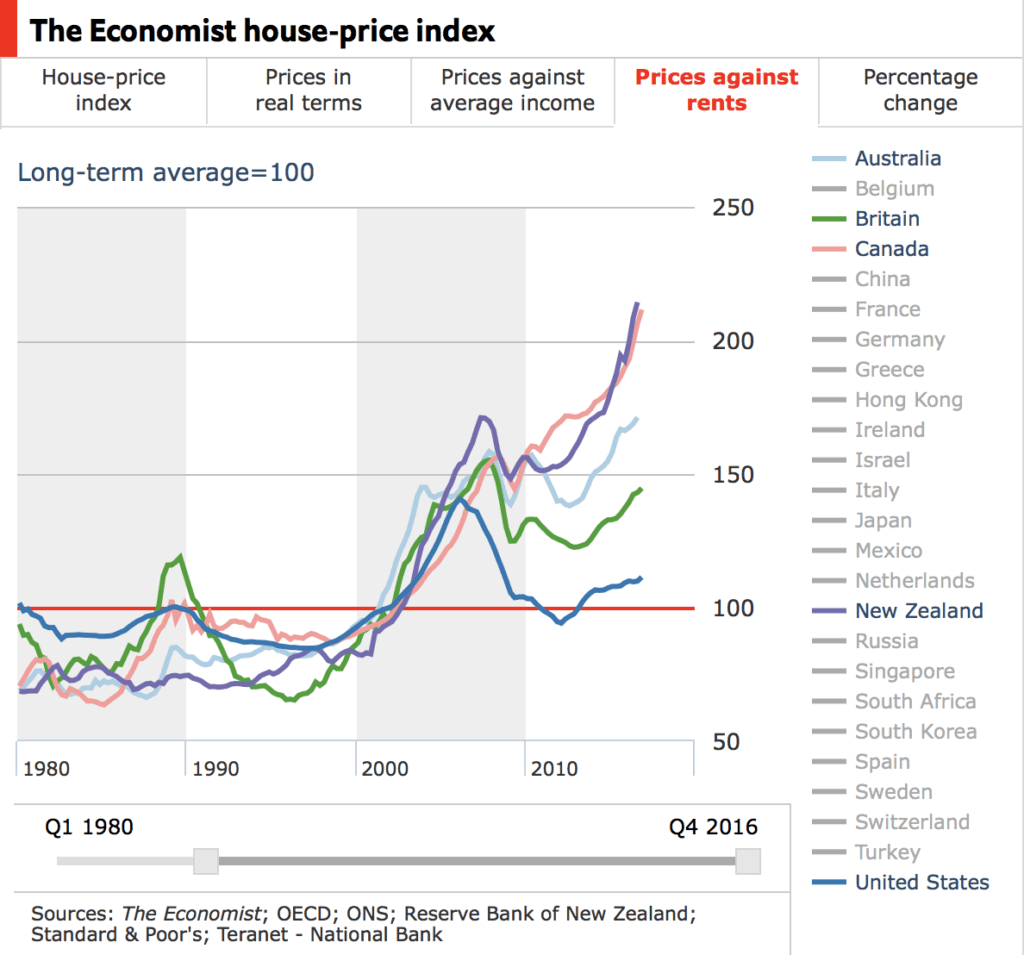

As investors we’re interested in viewing real estate as we would any investment or asset, and as such understanding the cashflows is important. Naturally, incomes relative to asset prices tell us what the owner’s cashflows are relative to the asset they’ve buying… and the same analysis can be conducted against student loans, car loans – any credit instrument, really.

Here’s rents (cashflows) relative to asset prices:

Oy vey! There’s enough there to make your hair stand on end.

What do you think the cashflows on this baby are like?

I wonder if it comes with free tetanus shots?

Spotting bublicious markets is one thing but it’s quite another identifying turning points and then another altogether finding a means of constructing an asymmetric payoff.

Here’s a question to ask yourself:

What happens when cap rates go from 4 to 6 as in the US and from 5 to 8 in a place like New Zealand? I think we’re going to find out over the next few years.

Napkin Math

Let’s do the math…

We’ll keep the numbers dead simple. It’s the same math as looking at the market cap of a company and its dividend yield and free cashflows.

So we’ve got an asset, a commercial building someplace priced at $1m with a 4% cap rate, thus yielding $40k, and let’s assume financing costs at, say, 4%. Now this mythical building could be in Toronto, London, Sydney, or Auckland. And yes, I know financing rates and cap rates differ across town let alone across countries but it doesn’t matter – the same principles apply.

Now, for the guy owning this asset he’s either:

- Levered and using the $40k to service debt, or…

- He’s simply allocating capital and the 4 cap rate was more attractive than the 2 he’d get on a CD.

You may ask yourself the question: Why on earth would an investor buy a 4 cap asset in an environment where financing costs are 4%?

After insurance, maintenance, any tenant vacancies, and other opex you’re definitely underwater. A great question and one that many investors are going to be asking themselves while staring in the mirror at some point in the next few years.

The answer actually lies not in math but in human behaviour and expectations.

When rates continuously moved lower and then lower still as coordinated global central banks held rates down, buying in anticipation of ever cheaper financing costs made a lot of sense. Plenty people have gotten very rich doing it over the last few years.

Even just a 25bp move on debt financing on a multimillion portfolio of assets translates into a a heck of a lot on the asset price revaluation. And what’s more is that the guys buying negative yielding assets woke up a few short years down the track to a situation where cashflows had turned positive (financing costs moved lower) on top of the price appreciation which has been enormous. That’s how leverage works and that’s how linear assumptions get made well into the future.

Now let’s get back to our story and say lending rates rise by 200bp to 6%. The market will immediately begin to reprice all assets, including our mythical commercial building.

What are we prepared to pay for this place in a 6 cap environment?

Our interest expense just went from $40k to $60k – a 50% increase.

$40k of income used to service $1m of debt but at a 6 cap it only services $666k – a nice 33% equity haircut.

Except, of course, that’s not at all how markets work.

They are forward looking, and so when the market finally figures out that financing costs (rates) are heading higher not lower for longer, then they begin pricing in this reality and cap rates go higher than financing costs, sometimes much higher. What happens to the equity? My guess is we’re going to find out.

On Friday I’ve got a follow up article from a good friend of mine, which gets into a particular sector of the market where this is likely to hit hard.

– Chris

PS: I normally have a poll on the WOW and today I don’t. They say a change is as good as a holiday, plus I’ve gotta keep readers on their toes.

Oh, and if you like… no, love Capitalist Exploits, then please share it with every man woman and child you know. I’ll love you even more.

“There are decades where nothing happens, and then there are weeks when decades happen.” — Lenin