Singapore is regarded as the “safe haven” or Switzerland of Asia. While on the surface Singapore is the economy to which most others can only aspire to one day become, beneath the scenes is a very fragile economy highly dependent on the cost of capital staying low or at least rising very slowly over the coming years. If rates in the US rise sooner than what everyone expects and by a greater magnitude, the Singapore economy and dollar are in big trouble!

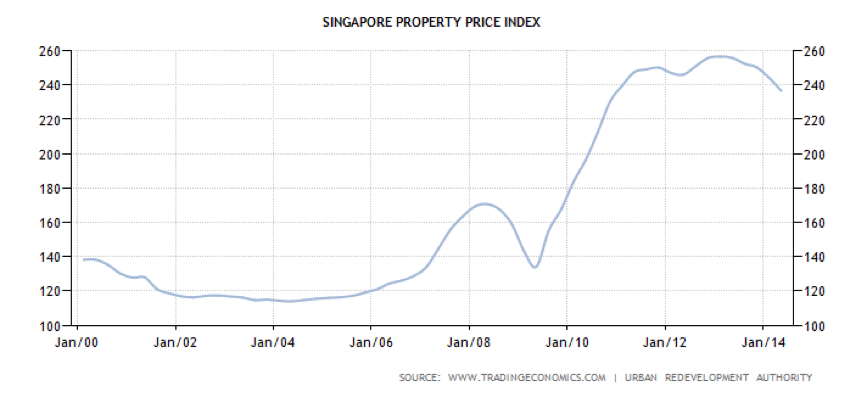

Let’s get straight to the point – Singapore has a huge problem and it relates to its property market – property prices have advanced some 50% since the start of 2006.

High property prices in themselves aren’t a problem. The problem is essentially the way in which the property market is financed, but more on that later.

What has caused this insane rise in property prices? From the chart above notice that most of the price movement occurred from 2009 to 2013. This was a period in which the US Fed engaged in what seemed an infinite “quantitative easing” program which took short-term rates down to virtually zero percent.

The Fed’s quantitative easing program has had far-reaching consequences for which it has openly stated that it doesn’t care (everything is ok as long as it is in the interests of the US). One way the stimulus manifests itself is as bubbles in other economies, particularly of the emerging variety, where the ultra-low rate set by the Fed has been exponentially compounding what was already a serious problem caused by China’s seemingly insatiable appetite for growth.

Singapore’s benchmark interest rate, the SIBOR, is tied to the U.S. Fed Funds Rate to minimize large swings in the exchange rate. Low interest rates are a direct cause of credit bubbles, and this is what is happening in Singapore.

Since the SIBOR is used to price the majority of loans and mortgages in Singapore, a very low SIBOR means cheap credit in Singapore. The ratio of household debt to gross domestic product now stands at around 77%, up from 55% in 2010 and 45% in 2005.

Furthermore, almost all mortgages in Singapore now have floating interest rates, meaning that once the Fed tapers, mortgage repayments will increase too, exposing unsustainable debt levels in the system. Let’s take a closer look at this stupidity.

The average mortgage rate in Singapore is now approximately 1%. This is ok as long as rates don’t move. Looking at the history of the fed funds rate, which was at 5% as recently as 2007, it has trended between 3% and 6% for the last several decades. If – or should I say when – Fed rates return to their historical averages after this exceptionally long period of low rates, Singapore’s housing market will discover a double whammy of underwater homes and unaffordable interest payments.

At 2%, interest payments in Singapore will more than overwhelm the principal and double monthly payments. It isn’t hard to see how disposable income and consumer spending in Singapore is so vulnerable to rising interest rates.

Singapore is not alone in its fragility to rising interest rates. What is happening in Singapore is a symptom of a broader macro theme (consumers gorging themselves on cheap credit). There is a region-wide emerging markets bubble, encompassing not just Singapore, but also Malaysia, Thailand, the Philippines, Indonesia, Australia and New Zealand. Singapore just happens to be the financial hub of the region and thus benefits from the skyrocketing price indices and booming household debt, as long as it lasts.

This emerging markets bubble is likely to burst, once the Chinese bubble and thus commodity prices pop (which they now appear to be doing). Given the makeup of Singapore’s economy, mainly characterized by finance and real estate, the chain of events could unfold in a way that echoes the financial crisis in Iceland and Ireland. However, as is usual with bubbles, they tend to be flat-out denied until they burst for little or no apparent reason.

The Economist labels Singapore as the third most expensive residential property market in the world, on a price-to-rent basis, causing a 60% overvaluation relative to the long-term average. Only Canada and Hong Kong are pricier. If the property market goes, so does the banking sector, since the banks hold almost 50% of their credit portfolios in property-related loans, residential mortgages making up nearly a third. Given that the vast majority of loans have floating rates, these banks are in for a horrible wake-up call on the bad loan front as rates rise.

The evolution of Singapore’s bubble is closely tied to US monetary policy, and though the causality is far from clear, Singaporean home price indices did reflect the first decline in seven quarters in 2013 Q4 and have been declining ever since, as the Fed started and continues to “taper”. Since the process of returning to non-zero interest rates in the US is likely to be extremely slow, the bursting of Singapore’s bubble is hardly imminent. However, there is always the risk that rates in the US rise sooner than expected because, if history is anything to go by, rarely do expectations match reality.

As the Fed moves towards raising rates, the risk must certainly be that rates rise sooner than expected. Why do I get the feeling that we are sitting precariously close to a repeat of the 1997 Asian Tiger crisis? If one of Singapore, Malaysia, Indonesia, the Philippines, Thailand, Hong Kong, or Australia or that matter gets into trouble then the rest go. Of course, I didn’t even need to mention China!

Expressing bearish views on the Singapore dollar is a great way to position for rising rates in the US and any crisis that is likely to materialize from rising rates. The preference is to express the view via long term call options on the USD/SGD.

– Brad

“The rising tide lifts all the boats.” – John F. Kennedy

This Post Has 11 Comments

Great article! So when the bubble finally does pop, do you think the Singapore property market will fall to where the prices at least appear to be reasonable?

Goodness knows what a “reasonable” level is or how long it takes to get down to that reasonable level. I’m not trying to be funny……reversals of primary trends in a market aren’t difficult to see coming but the extent of that reversal is somewhat impossible to predict. Anyway let me extend myself and say that real estate prices in Singapore are likely to be materially lower in a couple of years from now (and that is as close as I can get to a predictions).

This is the first time I hear you guys being negative on SE Asia.

I will not disagree with the fact that rising interest rates will hurt those who are over extended. And since everyone in Singapore seems to think lately that property prices can go nowhere but up, I sure believe some Singaporeans might have gotten a little carried away investing in property. However:

1. On your 1st property in Singapore I believe you need to make a down payment of 20%. 5% of which is cash, another 15% of which is either cash or comes out of your CPF, the mandatory national saving fund that every citizen has (+/- 36% of your salary goes in there). For a 2nd property the down payments needs to be 50%. This seems a lot more conservative than in the US.

2. Most Singaporeans will have savings, again because of this mandatory CPF. Technically, their monthly income could increase 45% if you were to count their contributions to the CPF as income. I see some margin of safety here.

3. Contrary to the US, the economy is actually growing at close to 4%. Entrepreneurs like to set up shop in Singapore because of the less stringent regulation and Oil&Gas companies move their APAC headquarters to Singapore because of its central location, good infrastructure, educated labour force and lower labour costs than in Australia. As long as they will continue to do so, the economy will continue to grow.

4. I honestly don’t know whether the huge current account surplus that Singapore has been running plays any role but it certainly won’t be bearish for the Sing Dollar.

5. Other than real estate, Singapore is still quite cheap and over time can make their currency appreciate to obtain a higher standard of living.

Last time I was in Singapore, it did look like there was a lot of new residential supply getting onto the market so real estate prices sure will go down at some point. I just don’t see their currency being any more vulnerable than the USD. I might be wrong.

The big attraction of the Singapore dollar is just how cheap the options are. Buying calls on the USDSGD are so cheap and the payoff so huge that the possibility of material upside in the USDSGD cannot be ignored.

Great wake up call to a potential pitfall on the SGD. We have of course been using it a a “safe haven” currency and also some of our core income holdings are the Sabana and Parkway REITs.

As Roojoo very cogently points out, perhaps there are buffers to a drop in property values and a rise in rates, within Singapore. I think it is the same for most individual property owners here in China (paid cash or low debt/equity), but it is obvious many developers are in WAY over their heads and the banks will be left holding the bag.

So is it time to sell Asian REITs? Is it time to sell SGD for USD (or HKD)?

Thanks to Chris and Mark for the continuing insights on the Asian markets!

Be very careful of any market that is referred to as a safe-haven. Once everyone refers to market as a safe-haven it is generally indicative of it being a “crowded” trade with lots of marginal sellers.

Long term call options on the USDSGD can hedge out a lot of risk that one is running re exposure to the SGD. And right now they are very cheap .