Market dislocations occur when financial markets, operating under stressful conditions, experience large widespread asset mispricing.

Welcome to this week’s edition of “World Out Of Whack” where every Wednesday we take time out of our day to laugh, poke fun at and present to you absurdity in global financial markets in all it’s glorious insanity.

While we enjoy a good laugh, the truth is that the first step to protecting ourselves from losses is to protect ourselves from ignorance. Think of the “World Out Of Whack” as your double thick armour plated side impact protection system in a financial world littered with drunk drivers.

Selfishly we also know that the biggest (and often the fastest) returns come from asymmetric market moves. But, in order to identify these moves we must first identify where they live.

Occasionally we find opportunities where we can buy (or sell) assets for mere cents on the dollar – because, after all, we are capitalists.

In this week’s edition of the WOW we’re covering Australian banks

A friend working at one of the big 4 Aussie banks sent me something which led to my pulling up the charts of the big 4. Whoah!

It blew me away because we have a collective head and shoulders top, something that should cause indigestion for any investors long the sector.

I want to bring to your attention the Commonwealth Bank (CBA) below what is sporting one of the biggest head and shoulders tops I’ve ever seen.

Not long ago I highlighted the good ol’ land down under suggesting that maybe, just maybe, Australian housing prices had diverged from reality. Perhaps, looking around the world at all the fun that could be had with unreasonably low interest rates, they felt lonely and wanted to join the party. In that article I pondered the following:

“I’m struggling to understand how an economy increasingly running on the over consumption of real estate financed by mortgage debt is anything but insane?”

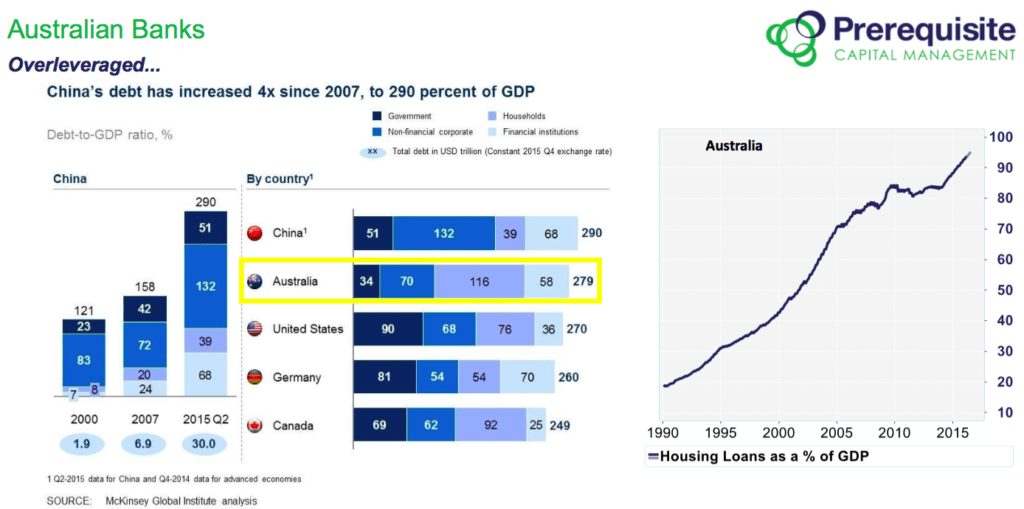

To understand Australia it’s useful to get a grasp on China. After all, when your biggest trading partner is experiencing a slowdown and at the same time your economy is increasingly being held up by investment in housing, then the odds are decent that risk in the system has increased.

We’ve previously covered China but let’s briefly take a step back in time to late 2014 when we dived into the interbank lending market in China and explained why the rapid rise in the interbank lending rates was likely a precursor for the direction of the currency and problems in their banking sector.

“Rapid rises in interbank lending rates are often associated with banking or credit crisis.”

Just four months later the renminbi was officially devalued, followed by successive devaluations which I’d assured you were coming. This was simply connecting the dots to develop an understanding of the consequences and knock on effects of a tightening interbank lending market and how this manifests itself in other ways.

Today we sit at 6.69 up from 6.12 when we published that article. For investors riding this trend, it’s been more fun than watching a string bikini parade.

So what does this have to do with Aussie banks?

If we look at the underlying problems and causes for China’s woes, the rapid increase in leverage in the banking system stands tall and mighty. It was after all the tightening in China’s interbank lending market back in late 2014 which first alerted us to the problems we subsequently found lurking below the surface.

China is important to understand as it relates to Australian banks for two reasons:

- China’s credit woes look eerily similar to those being exhibited by the lucky country, and…

- China is Australia’s largest trading partner. A slowdown in Chinese consumption therefore directly affects Australia.

In my research on Australian banks I came across an excellent analysis by Daniel Want at Prerequisite Capital Management in Sydney. I have yet to meet Daniel or the folks at Prerequisite but next time I’m in town I plan to offer to take him out to dinner because his work is excellent. Daniel highlights many of the core issues in the Australian economy, pointing out that Australia is at the top of its credit cycle, which has been significant by any standards.

We can see that Australia’s economy is over-leveraged, though we also know that this has been a condition of the sick patient for some time.

Why Now?

The two components to leverage are aggregate debt, and the cost of carrying that debt. We know that aggregate debt has been steadily rising since the GFC, a problem I might add which has been wonderfully masked by absurdly low interest rates meaning that at the same time the cost of carrying that debt has been steadily falling. What’s to worry about?

This collapse in funding costs over the last 10 years has provided gasoline to the housing bubble fire built on cheap credit. No sector is more closely tied to the Australian housing bubble than the big 4 Australian banks.

Funding Environment

Australian banks are price takers. This is to say that a substantial amount of the banks funding is sourced offshore. We are experiencing what we believe to be the beginning of a significant shift globally to tightening liquidity conditions. There are many factors contributing to this, some of which I’ve spilled ink on previously (rising nationalism and protectionism and others which are more quantitative in nature). The scope of this article isn’t sufficient to cover those topics.

Suffice to say that as global liquidity tightens Australian banks will find it increasingly costly to finance and they will need to pass those costs onto…you guessed it. The household. Households who are unprepared for rising rates.

But Australia Hasn’t Had a Recession for 25 Years!

And that means they’ll never again in the history of mankind experience one, right?

Herein lies the problem. We poor humans think in a linear fashion while we live in a dynamic world. It’s no wonder we act so irrationally. Predictably irrationally I might add. As the market has grown, without a recession to correct excesses so too has the banking sector. A sector of the economy which employs vast amounts of leverage. This is of course a global problem and not one isolated to Australia, however it has the potential to affect Australian banks more acutely than other developed market banks should liquidity tighten globally as appears to be happening.

Daniel takes another metric which I think is useful when valuing the big 4 Australian banks. The ratio between the average Australian income, and that of the market capitalisation of the big 4 banks.

“Banks are currently valued at about 37% of a working age person’s average income (up from only 7% 25 years ago)”

Readers will know that Australian household debt to GDP is now over 123%, one of the highest on this ball of dirt. And the combination of this and a tightening in global liquidity doesn’t bode very well for Australia’s banks.

If there is to be one culprit in this story it is undoubtedly those men and woman in plush offices with Chivas on tap, debating how many trillions of dollars they should or shouldn’t be pouring down the drain of our future, believing they have colossal brains able to deal with problems which they’re too arrogant to admit are of their own making. We call them central bankers and they have created some of the most amazing investment opportunities we’re likely to ever see. It is a shame that most won’t benefit from what is likely to be a blip on the long term history of financial markets but will rather become victims.

Australian banks are joined at the hip with the Australian real estate bubble and a combination of factors threaten to cause problems for them over the coming few years.

In part of this article we looked back on an article written about the devaluation of the renminbi. Will I be writing another article in a few years, looking back on this very article today, after we’ve seen loan impairments hit the sector and the market cap of these big boys trimmed from where they are today? Stranger things have happened. Maybe it’s time to position accordingly.

[yop_poll id=”21″]

Know anyone that might enjoy this? Please share this with them.

Investing and protecting our capital in a world which is enjoying the most severe distortions of any period in mans recorded history means that a different approach is required. And traditional portfolio management fails miserably to accomplish this.

And so our goal here is simple: protecting the majority of our wealth from the inevitable consequences of absurdity, while finding the most asymmetric investment opportunities for our capital. Ironically, such opportunities are a result of the actions which have landed the world in such trouble to begin with.

– Chris

“I’m more than content to lower it if that actually helps but is that the best thing to do at any particular time? We’ve got Christmas. We should just chill out, come back and see what the data says.” – Glenn Stevens, RBA Governor on the prospect of an interest rate cut