The more we look at the Chinese renminbi the more convinced we become that the next serious move will be to the downside and that this will more than likely occur sooner rather than later.

Last month I wrote an article “The World’s Biggest Asymmetric Trade Just Got Bigger”. This is an update to that article where I look at developments in interbank lending markets which will no doubt set off alarm bells! Alarm bells if you haven’t got any bearish exposure to the renminbi and, if you already have an exposure, question whether or not you have enough!

Before I start talking about the interbank lending market in Chinese renminbi let me talk a little about the interbank market. The interbank market is simply a market at which banks can enter to borrow or lend US dollars to each other, it is also known as the wholesale market.

The interbank lending market is an integral part of any country’s banking system as it is where banks maintain their short-term liquidity requirements. Often a bank will have a mismatch between between short-term assets and obligations and as such they will have to enter the interbank lending market to maintain optimal liquidity. If a bank has excess short-term reserves they may want to lend these out to other banks who have a shortfall in short-term reserves. The opposite also occurs where a bank, with a short-term funding deficit, will enter the market to borrow funds to match short-term liabilities.

The behavior of the interbank lending market can provide one with a good appreciation for the liquidity of the banking system as a whole. If there is a lot of liquidity in the system (more short term assets than liabilities) the interbank rate will fall, if there is scarcity of short term assets relative to liabilities then rates will rise. So a rising interbank rate is generally associated with contracting liquidity conditions. Rapid rises in interbank lending rates are often associated with banking or credit crisis. This happened in the lead up to the GFC. What happened was that as banks began to fear the ability of other banks, who are their counter-parties, to make good on their obligations they demanded higher rates especially from banks already facing liquidity problems which only compounded their original the situation.

A rapid rise in a country’s interbank lending market is also a good predictor of the direction of a country’s currency, or at worst a confirming indicator. Let’s have a look at the interbank lending market of a few emerging nations over the last 12-18 months and then look at what is happening with the renminbi. I think it is instructive for what we have been positioning for in our funds.

The Malaysian Interbank rate (KLIBOR) has been rising consistently since late last year and now the Malaysian ringgit is going parabolic (the ringgit is collapsing against the USD).

KLIBOR 3-month rate (blue) and Malaysian ringgit (yellow)

KLIBOR 3-month rate (blue) and Malaysian ringgit (yellow)

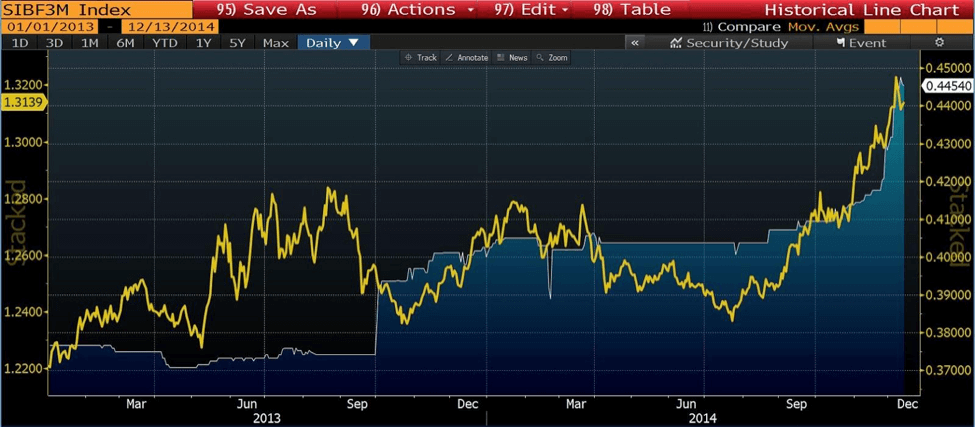

The Singapore 3-month SIBOR first jumped in over a year ago and as of the last few months has started to rise in a parabolic fashion with the Singapore dollar in tow. As with the ringgit above the Singapore dollar is falling against the USD.

SIBOR (blue) and Singapore dollar (yellow)

SIBOR (blue) and Singapore dollar (yellow)

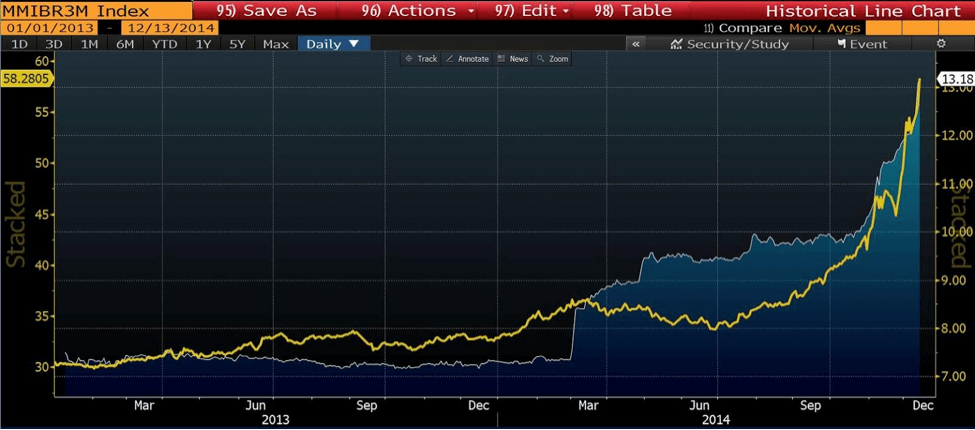

The Russian ruble has been rising for the last couple of years but started to go parabolic when the Moscow interbank lending rate (MIBOR) exploded to the upside, or was that the other way around? It’s difficult to identify what is cause and effect, but one thing for sure – big blow out in currencies tend to occur when the interbank lending rate is rising rapidly.

MIBOR 3-month rate (blue) and ruble (yellow)

MIBOR 3-month rate (blue) and ruble (yellow)

Now this is the situation with the renminbi. The HIBOR (CNH) 3-month rate is going parabolic, although the offshore renminbi (quoted USD/CNH) is only up marginally since the HIBOR rate took off a few weeks ago, if the HIBOR rate continues to climb then I think it is a “certainty” that the USD/CNH will play catch up – i.e. get ready for a big move to the upside!

HIBOR (CNH) 3 month rate (blue) and USD/CNH (yellow)

HIBOR (CNH) 3 month rate (blue) and USD/CNH (yellow)

While I am not 100% wedded to “technical” analysis, I know a bullish chart pattern when I see one, or at least one in the making. If the USD/renminbi can register a multi-month high, a very significant bullish signal will be generated. I am confident that this will happen over the coming days.

So we’re expecting a big move to the upside in the USD/renminbi but option writers don’t appear to be. The cost of long-term options (implied volatility) on the USD/CNH still appears to be very cheap, although the last few days has seen a sharp jump higher. We think the best way to apply a bullish view on the USD/CNH is via long-term call options.

USD/CNH implied volatility for ATM 12-month to expiration options

USD/CNH implied volatility for ATM 12-month to expiration options

Over the last 6 months, we have been quietly gearing ourselves up for a dramatic move to the upside in the USD/renminbi. As interbank lending rates in emerging markets started to explode higher over the last 6 weeks we have picked up our pace of buying long term FX call options on the USD/renminbi. 12 months from now I suspect our only regret will be not being aggressive enough.

– Brad

“I’d rather regret the things I’ve done than regret the things I haven’t done.” – Lucille Ball

This Post Has 31 Comments

Hi Brad, for US citizens, how would you recommend we trade this? RMB future options on the CME have zero liquidity; the futures have a little.

Any suggestions would be appreciated!