Market dislocations occur when financial markets, operating under stressful conditions, experience large widespread asset mispricing.

Welcome to this week’s edition of “World Out Of Whack” where every Wednesday we take time out of our day to laugh, poke fun at and present to you absurdity in global financial markets in all it’s glorious insanity.

While we enjoy a good laugh, the truth is that the first step to protecting ourselves from losses is to protect ourselves from ignorance. Think of the “World Out Of Whack” as your double thick armour plated side impact protection system in a financial world littered with drunk drivers.

Selfishly we also know that the biggest (and often the fastest) returns come from asymmetric market moves. But, in order to identify these moves we must first identify where they live.

Occasionally we find opportunities where we can buy (or sell) assets for mere cents on the dollar – because, after all, we are capitalists.

In this week’s edition of the WOW we’re covering the Japanese central bank policies and the recent rise in Japanese interest rates

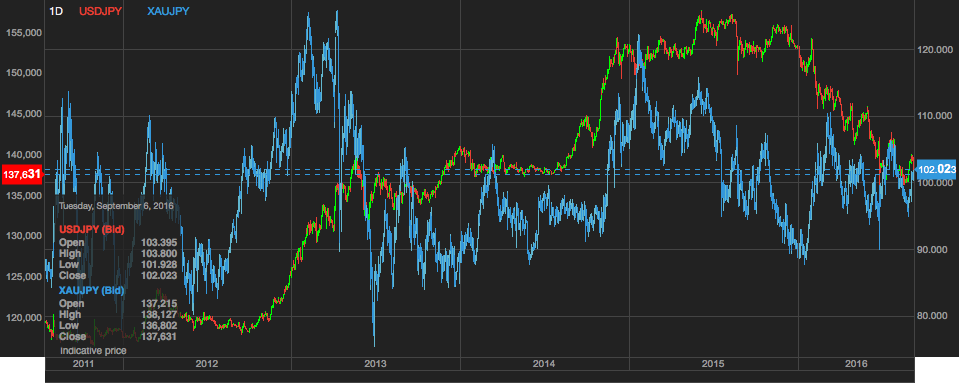

It was back in mid 2011 that I first began shorting the yen. Specifically, I was long both XAU/JPY (in blue) and USD/JPY (in green and red).

On the USD/JPY we moved all the way from 72 to 125 in early 2015 which was obviously a profitable run.

Gold, on the other hand, went ballistic through late 2012, then proceeded to collapse into 2013 before bouncing back and settling into a trading pattern (albeit a volatile one) which is pretty much where we stand today.

I’ve been trading around these core positions ever since I first poked fun at the BOJ in March of 2011.

Then the following year (January of 2012) I wrote a satirical piece, suggesting methods the BOJ could use to entice retail investors into the JGB market. Ironically my satire today looks far more plausible than the methods subsequently taken by the BOJ over the last 4 years. Truth truly is stranger than fiction.

Beginning 2016 the USD/JPY positions have experienced significant drawdowns with volatility spiking. Drawdowns only hurt if you’re levered, while volatility is important for that portion of any position held in options contracts. You want to be buying volatility when it’s cheap and selling it when it’s expensive.

I mention these things since I’ve been looking to re-establish and pyramid back in. And so as I sit here today I’m left pondering the BOJ’s next move and how much manoeuvrability they have left.

Japanese government bond rates have been rising sharply towards the zero mark over the past 6 months. A reversal of the downtrend. We can see this in the 10-year JGB chart below.

This is causing concern amongst the elites at the BOJ. Like market participants such as myself and many of the fund managers (some of the world’s most notable and successful) I regularly speak with, the BOJ may be asking the same question we are: is this the invisible hand of the market beginning to repudiate negative interest rates?

We’ll only know in hind sight and must work with the probabilities in any given scenario. I know of no successful trader or investor who manages risk any other way.

What Will the BOJ Do Next?

In a recent statement Kuroda-san dismissed ideas of calling a halt to their aggressive monetary policy, and while what a central bank says and what a Central bank does are not always the same thing, we do know that the BOJ is in a bit of a pickle.

“It is often argued that there is a limit to monetary easing, but I do not share such a view.

Needless to say, there is still ample room for further cuts in the negative interest rate and for an increase in the quantity dimension.”

The BOJ Conundrum

Do you remember the Monty Python skit with Colin “Bomber” Harris self-wrestling where he succeeds by defeating himself?

The BOJ is the “Bomber Harris” of the central bank world. It’s gotten to the point where it is wrestling with itself and bound to win, and in doing so bound to lose.

They’ve stated their intent purpose is to create inflation. It’s not specifically to destroy the yen or further layer the country with ever greater debts. It’s to create inflation. They are simply accepting that those are the consequences they must bare.

The process which they’ve used to do so is with a record-setting bond purchase program which has now crept into buying equities and commercial property ETFs.

Consider that the former (bond purchasing) was designed to push interest rates down, forcing capital out of the bond market into the equity markets. Forcing people to essentially spend and invest instead of hoard and save, thus stoking the flames of inflation.

The latter (buying equities and commercial real estate ETFs) has been a panicked attempt to do what the market has largely refused to do in the size deemed necessary as the 2% inflation target still looks a long way off.

This is self-wrestling at its best. As bond yields have plunged below the neckline, destroying the ability of savers to get any sort of return those savers have instead saved more and hoarded money. Deflation is persistent as a result.

Many of you will remember my conversation with colleague Grant Williams early this year where we discussed the market reaction to the BOJ going negative. The Nikkei dropped at the open and the yen rallied. Not at all what the BOJ expected or wanted. Wrestling against themselves.

As I mentioned in a recent issue of World Out of Whack focused on demographics, consumption changes radically when you’re retiring. Needs change and that is a qualitative issue that few seem to grasp, certainly not central bankers.

While these policies continue to fail, the debt pile grows and tensions increase. A consequence of enormous debt is the ability to service these debts. Nobody is talking about this anymore. At negative interest rates who cares, right?

The Three Musketeers

In a world where central bank policy globally is co-ordinated, negative interest rates don’t seem to pose much risk. Provided they’re all in it together. One for all and all for one.

The ECB, FED, and BOJ are of course the three most important central banks in the world and the only real players when it comes to deep liquid capital markets.

It’s ironic that the BOJ is using negative interest rates in an attempt to devalue the yen but can only really be successful if they can devalue against the euro and dollar.

This means of course that a yen devaluation needs to be met with either no or less devaluation by the ECB and the FED, otherwise it simply doesn’t work as they all go down together.

And herein lies the conundrum. Co-ordination between these three musketeers is necessary in order for the bond markets to hold together. Breaking ranks could provide a global shock that markets are wholly unprepared for and as the entire ball of wax grows bigger, any divergences become more and more dangerous. Pretty soon the smallest arbitrage will threaten to tear through the increasingly fragile markets.

Interestingly this is where the qualitative, not quantitative side to economics becomes really, really important. It’s a reason why I’ve been hammering on about the change in the zeitgeist affecting US politics as well as the changes taking place in European politics. These are qualitative behavioural economics issues which, together with the quantitative, need to be understood (a topic I’ll be covering later this week).

Rates or Currencies? Take Your Pick

So on the one hand we have currency risk and on the other we have interest rate risk.

Right now interest rates are negative with the outlier being the US. If the chubby lady hikes, even by 25 basis points (because that’s the most they’d dare to do), then the BOJ will get what they want in a depreciating yen. But the consequences to their already falling bond market (rising rates) could get out of hand and quickly.

Ironically the easiest way to counter that would be for the Fed to slash rates, bringing rate differentials closer together but that would not have the same depreciating affect on the yen.

What is clearer with every passing day is that these guys are less and less data dependent. Monetary policy at the BOJ is now completely reactionary and chaotic. After all, what’s the point at looking at data sets anymore when any reference point that may have had any meaning was left miles offshore a long time ago?

Understanding where institutional capital will flow is always a pretty useful question and so..

Imagine you’re an institution (as some readers are) and have to buy government debt in size…

[yop_poll id=”20″]

Know anyone that might enjoy this? Please share this with them.

Investing and protecting our capital in a world which is enjoying the most severe distortions of any period in mans recorded history means that a different approach is required. And traditional portfolio management fails miserably to accomplish this.

And so our goal here is simple: protecting the majority of our wealth from the inevitable consequences of absurdity, while finding the most asymmetric investment opportunities for our capital. Ironically, such opportunities are a result of the actions which have landed the world in such trouble to begin with.

– Chris

“Oh what a tangled web we weave, when first we practice to deceive” – Sir Walter Scott