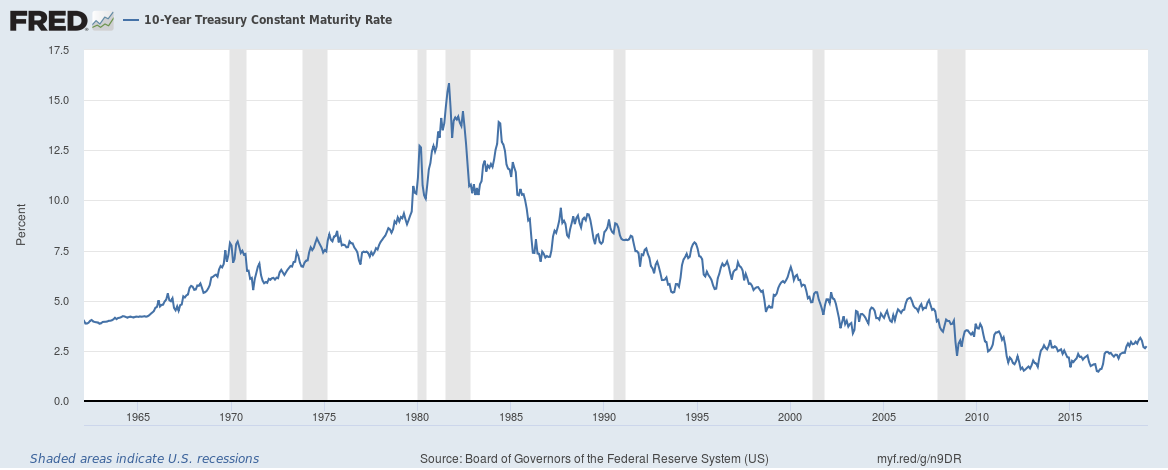

Let’s analyse the formation of the bond bull market which began in 1982. We’ll use the US 10-year as proxy. Here it is in all its glory:

The 60’s and 70’s saw bond yields run from a low around 4% to over 10% at the tail end of the 70’s. For bond bulls this was a period of time more painful than being trapped in a car listening to Mariah Carey for 3 hours straight (I had a torturous childhood and still wake in a cold sweat sometimes).

The inflation crowd had the reigns and rates ran and ran with bonds getting absolutely torched

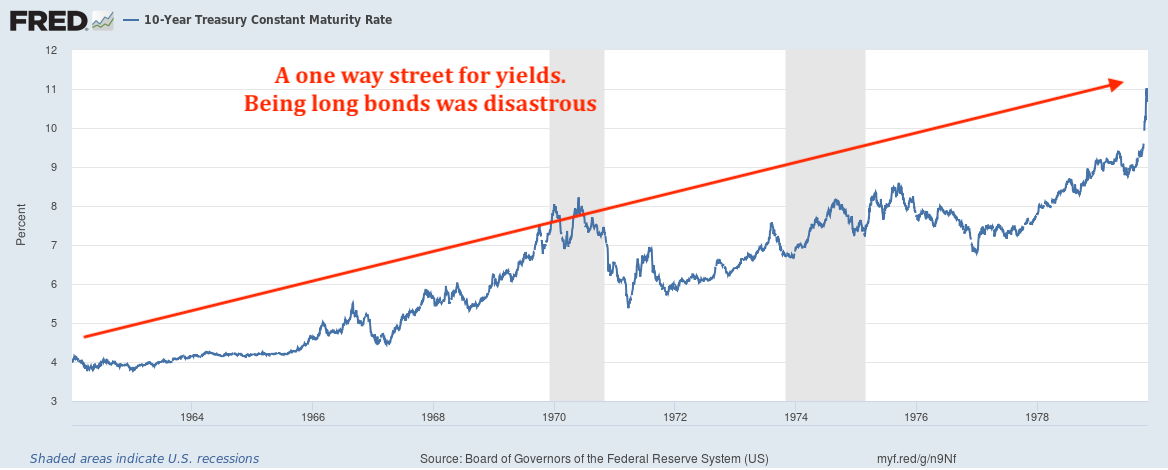

…and then BAM!

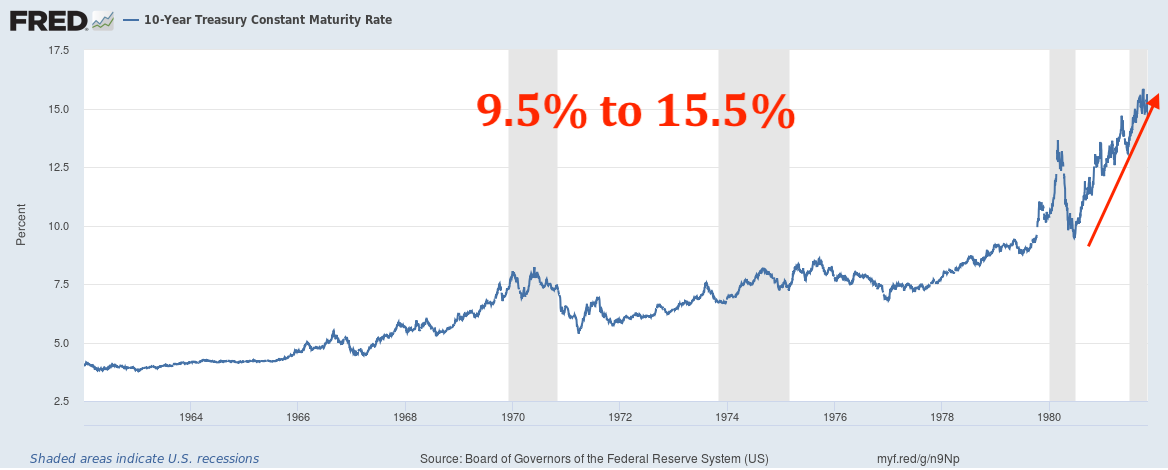

Bonds came out of the gate like they’d been juicing on steroids while training with Ben Johnson on the sly. Yields collapsed from just over 13% on February 22nd 1980 to 9.5% on June 20th. Only 4 months! A massive move in the scheme of things.

Now, to be fair, I wasn’t there when all this happened as I was still just a young snot annoying my mother. But I’m pretty darn sure that this move would have brought a few questioning folk over to the “inflation is no longer the risk” camp. But likely not many.

It also would have given pause to the bond bears. A little of that, ”Holy mother of Mary! What the hell? That wasn’t meant to happen!!” certainly crept in there. Which is, of course, what happens when you’ve been short bonds with leverage and just got margin called (and you can bet your hat many were leveraged short bonds because hey look, it’s been profitable for so damn long).

It’s an observable truth that leverage typically rises as market participants’ confidence in linear trends coincides with those same trends, despite fundamentals having already changed. We humans just can’t help ourselves.

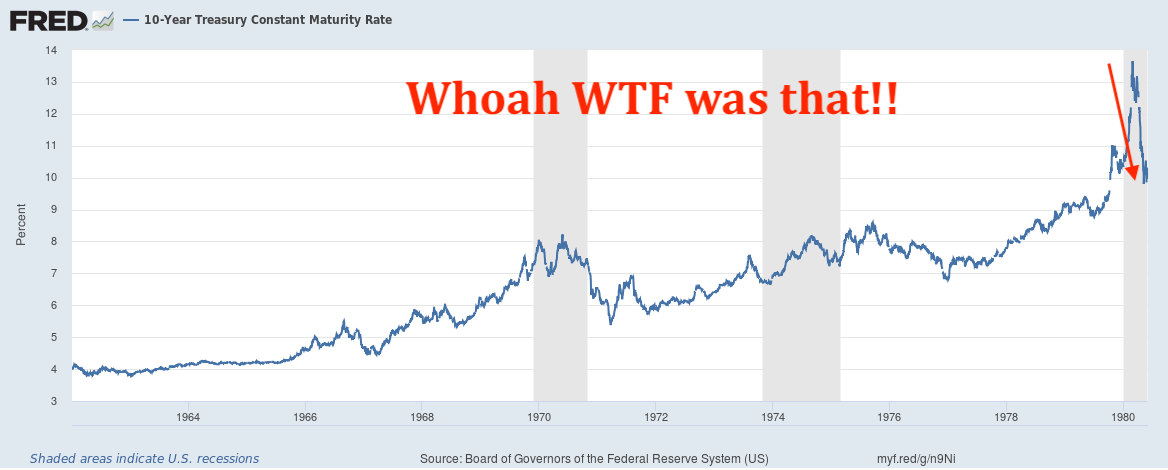

The very few bond bulls out there thought, “Hey, this is it!”. They were finally going to get some luvin’ as they’d got more than a fleeting glance. There was a flash of a thigh and a wink from their bond positions.

But then, just as they began congratulating themselves, their long positions promptly got up and ran out the door, but not before throwing their drinks in the bulls’ face. Bonds got hammered as yields ran like the police were after them. From 9.5% in June of 1980 to close at 15.65% on September 28th, 1981.

That’s a 6 percent move in just over a year!

Think about it like this. If you had (sensibly) moved some of your portfolio into bonds locking in stunningly high yields (and remember, yields had gone parabolic end of 1979 though February 1980), you’d have been validated for 4 months.

And you’d have been right, only to then see those gains wash away and yields rocket higher still. Mariah Carey was back wailing and screeching inflicting pain again.

Would you have reviewed what was going on or bailed as you stared at the red ink in your bond allocations? It’s a tough question because obviously you couldn’t have known the future. You had to rely on your own analysis of the various moving parts and make a call.

In hindsight, holding onto what was sensible was the right call, but I wonder how many had the fortitude to do just that.

Those that did had the next major shift nailed, and they didn’t have to do a whole lot more for the next 40 years.

When I say that the bond market is THE most important market out there, I hope this highlights that.

The thing is the expectations of market participants are formed and formulated by the experiences of the previous trends. And we’ve had a 40-year trend, folks. That’s really quite something.

And to be clear, it’s come at a tremendous price and to keep it going we’ve had the most insane monetary shenanigans the world’s ever seen. Period.

Has it stopped cycles? No more than putting out forest fires every time they start makes it “safe” in the short to medium term while allowing the dry underbrush to build up to the point where an unstoppable scorch the earth fire rages.

We humans can’t help ourselves. Getting ever increasingly complacent and comfortable as cycles mature and ever more fearful of whatever it is that’s been out of favour.

Here at Capitalist Exploits we’ve been rather vocal about the many indicators telling us that the bond market has already topped out.

We can see that the last 4 months have seen the good old questioning taking place as bonds have rallied causing those of us who are synthetically short via multiple strategies. Coincidentally anything that does well with bonds doing poorly has done…well – poorly. It’s painful but really we should expect this.

Two Generations in

It’s worth remembering that we’ve now two generations of fund managers, analysts, mutual funds, and asset managers of all stripes who’ve lived through nothing but a collapsing yield curve. It’s the only thing they’ve ever known.

Realise that this means that the entire matrix of asset allocations has been influenced by the bond bull market. Every allocation considered whether it be to equities, corporate bonds, EM, Sovereign debt and commodities has been made in this environment. It’s like growing up in the tropics and believing the entire earth experiences nothing but hot, humid conditions. Nobody told you about this frightening world that involves snow, ice and conditions which will kill you if you’re exposed.

Hell, today we’ve still got pension funds running scenarios which paint a 7% annualized yield well into the future. You have to ask yourself the question, what the hell are they smoking?

Aside from the fact that the trend is clearly in the other direction for bonds, to actually achieve such a consistent return is mathematically impossible. I mean, have these folks looked at government and corporate bonds before forecasting such returns and building entire insurance and pension fund models on it? They can’t have. But hey, that’s been the returns over the last 40 odd years, so why not, right?

Over the next decade we’re going to see governments, asset managers, and Joe Sixpack grapple with the myriad fallouts that come with a regime change.

Ben Hunt said it best recently:

-Chris

“The past can’t hurt you anymore, not unless you let it.” ― Alan Moore, V for Vendetta